403(b) Retirement Plans: A Comprehensive Guide for Public School Employees and Non-Profits

Picture this: You’re approaching retirement, and you’re looking back on a long and fulfilling career in public education. You’ve made a difference in countless lives, but now it’s time to think about your own financial security. Enter the 403(b) retirement plan, a valuable tool that can help you save for the future while reducing your tax burden.

What is a 403(b) Retirement Plan?

A 403(b) plan is a tax-advantaged retirement savings account designed specifically for employees of public schools and certain other non-profit organizations. Similar to its counterpart, the 401(k) plan, a 403(b) plan allows you to set aside a portion of your pre-tax income for retirement. These contributions are not taxed until you withdraw the money, potentially reducing your overall tax liability.

Unlike 401(k) plans, 403(b) plans are offered by non-profit organizations rather than for-profit companies. This distinction means that 403(b) plans are subject to different regulations and contribution limits.

How Does a 403(b) Plan Work?

Contributing to a 403(b) plan is a smart financial move that can help you achieve your retirement goals. Here’s a breakdown of how it works:

* **Eligibility:** Public school employees and employees of certain non-profit organizations are eligible to participate in a 403(b) plan.

* **Contributions:** You can contribute a portion of your salary, up to the annual contribution limit, on a pre-tax basis. This means that your contributions are deducted from your paycheck before taxes are taken out.

* **Tax Advantages:** Your contributions grow tax-deferred, which means you won’t pay taxes on them until you withdraw the money in retirement. This tax-deferred growth can make a significant difference in the long run, as your investments have more time to compound.

Advantages of a 403(b) Retirement Plan

There are several advantages to opening a 403(b) retirement account:

* **Tax Savings:** Reduce your current tax liability by contributing pre-tax dollars to your 403(b) account.

* **Tax-Deferred Growth:** Your investments grow tax-free until you withdraw them, allowing your money to compound faster.

* **Employer Contributions:** Some employers may choose to make matching contributions to your 403(b) plan, further boosting your retirement savings.

* **Flexible Withdrawal Options:** You have the flexibility to withdraw your savings once you reach retirement age, without penalty. However, you may have to pay taxes on the withdrawals.

What is a 403(b) Retirement Plan?

403(b) retirement plans are tax-advantaged savings plans designed specifically for certain employees who work for public schools and certain other tax-exempt organizations. Much like 401(k) plans offered by many for-profit companies, 403(b) plans allow employees to contribute a portion of their paycheck on a pre-tax basis, reducing their current taxable income. This money is then invested and grows tax-deferred until it is withdrawn in retirement.

Benefits of a 403(b) Plan

There are several key benefits to participating in a 403(b) retirement plan. Here’s a closer look at each:

Tax-Deferred Growth

One of the biggest advantages of a 403(b) plan is the tax-deferred growth it offers on investments. Contributions are made pre-tax, meaning the money is deducted from your paycheck before income taxes are calculated. This can create significant savings by lowering your current tax liability and allowing your investments to grow faster over time.

Potential Tax Savings Upon Retirement

In addition to tax-deferred growth, 403(b) plans offer the potential for tax savings upon retirement. When you retire and begin taking withdrawals from your 403(b), the money is taxed as ordinary income. However, since you have already paid income taxes on the money when you contributed it, the tax you owe on your withdrawals will be lower than if you had invested in a taxable account.

Additional Benefits

In addition to the tax advantages, 403(b) plans offer a number of other benefits, including:

- Employer contributions: Many employers offer matching contributions to their employees’ 403(b) plans, which can help boost your savings even more

- Loan options: Some 403(b) plans allow you to borrow money from your account for certain expenses, such as buying a home or paying for medical bills

- Investment flexibility: 403(b) plans offer a wide range of investment options, allowing you to customize your portfolio based on your risk tolerance and retirement goals

403(b) Retirement Plans: A Guide to Saving for the Future

A 403(b) retirement plan is a tax-advantaged savings plan for employees of public schools and certain other tax-exempt organizations. Contributions to a 403(b) plan are made on a pre-tax basis, reducing your current taxable income. Earnings on your investments grow tax-deferred until you withdraw them in retirement, when they are taxed as ordinary income. 403(b) plans offer several benefits, including:

*

*

*

If you are eligible to participate in a 403(b) plan, it is a great way to save for retirement. However, it is important to understand the contribution limits and other rules that apply to these plans.

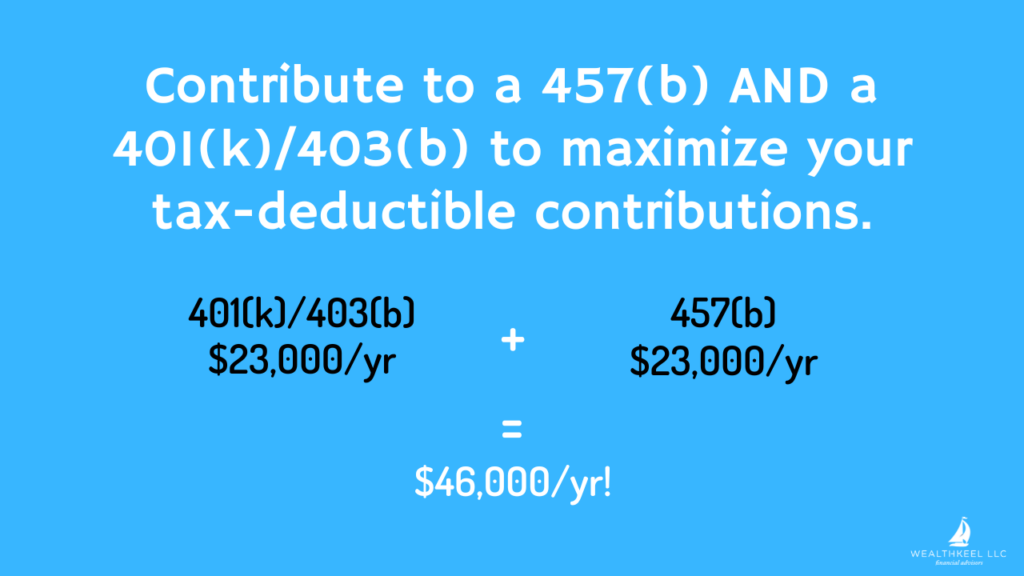

Contribution Limits

The annual contribution limit for 403(b) plans is set by the IRS and is typically adjusted each year. For 2023, the contribution limit is $22,500. However, you may be eligible to make catch-up contributions if you are age 50 or older. The catch-up contribution limit for 2023 is $7,500.

In addition to the annual contribution limit, there is also a lifetime contribution limit for 403(b) plans. The lifetime contribution limit is the total amount of money that you can contribute to all of your 403(b) plans over your lifetime. The lifetime contribution limit is $57,000, or $63,500 if you are age 50 or older.

It is important to note that the contribution limits for 403(b) plans are different from the contribution limits for other retirement plans, such as 401(k) plans. If you contribute more than the annual contribution limit to your 403(b) plan, you will be subject to a 10% excise tax on the excess contributions.

Employer Contributions

Many employers offer matching contributions to their employees’ 403(b) plans. These contributions are made on a pre-tax basis, reducing your current taxable income. Employer contributions are not subject to the annual contribution limit, but they are subject to the lifetime contribution limit.

If your employer offers a matching contribution, it is important to take advantage of it. This is free money that can help you save for retirement. You should contribute enough to your 403(b) plan to receive the full matching contribution from your employer.

Investment Options

403(b) plans offer a variety of investment options, including mutual funds, stocks, and bonds. You can choose the investments that are right for you based on your investment goals and risk tolerance. It is important to diversify your investments so that you are not too heavily invested in any one asset class.

If you are not sure how to invest your money, you can seek advice from a financial advisor. A financial advisor can help you create an investment portfolio that meets your individual needs.

A 403(b) Retirement Plan: A Path to Financial Security

A 403(b) retirement plan is a tax-advantaged savings plan designed specifically for employees of public schools and certain other tax-exempt organizations. This type of retirement account offers a range of benefits, including tax-deferred growth, potential employer contributions, and the ability to save for the future. Whether you’re a teacher, a librarian, or work for a nonprofit, understanding the intricacies of a 403(b) plan can empower you to make informed decisions about your financial future.

Employer Contributions

Often, employers recognize the value of their employees’ financial well-being and offer matching contributions to their 403(b) plans. This means that for every dollar you contribute to your account, your employer may contribute an additional amount, up to a certain limit. Employer matching contributions can significantly boost your retirement savings, so it’s crucial to take advantage of this benefit if it’s available.

Types of Employer Contributions

There are two primary types of employer contributions: matching contributions and profit-sharing contributions. Matching contributions are made on a dollar-for-dollar basis, up to a specified percentage of your salary. Profit-sharing contributions are made from the employer’s profits and are not tied to your individual contributions.

Eligibility for Employer Contributions

Eligibility for employer contributions varies depending on the plan’s specific rules. Some employers may require employees to meet certain criteria, such as length of service or age, before they become eligible for matching contributions. It’s important to check with your employer to determine your eligibility and the contribution limits that apply.

Maximizing Employer Contributions

To maximize your employer’s contributions, consider contributing as much as you can afford to your 403(b) plan. This will not only increase your potential retirement savings but also ensure that you’re taking full advantage of your employer’s matching contributions.

The 403(b) Retirement Savings Plan: A Comprehensive Guide

It’s like a secret savings stash that’s just for you—the 403(b) retirement plan. Just like a 401(k), this plan is designed to help you save for your golden years, offering tax advantages that’ll make you smile. But before you dive right in, let’s take a closer look at what it entails.

Investment Options

What’s the fun in saving if you can’t choose how to make your money grow? 403(b) plans usually have a buffet of investment options to choose from, like mutual funds and annuities. Mutual funds are like baskets filled with different stocks or bonds, while annuities are contracts that promise to pay you a steady income stream in retirement. The choices are plentiful, giving you the flexibility to tailor your investments to your risk tolerance and financial goals.

Contribution Limits

How much can you tuck away into your 403(b)? That depends on the rules set by your employer and the IRS. In 2023, the maximum you can contribute to your 403(b) is $22,500 (or $30,000 if you’re 50 or older). Plus, your employer can also make contributions on your behalf, known as "matching contributions." It’s like having a secret ally helping you save for your retirement.

Tax Benefits

Here’s where the magic happens. Contributions to a 403(b) are made pre-tax, meaning they’re deducted from your salary before income tax is calculated. This can save you a bundle come tax time. Plus, your investments can grow tax-deferred, meaning you won’t pay taxes on the earnings until you withdraw them in retirement. It’s like having a cozy tax haven right inside your 403(b).

Withdrawal Rules

Retirement might seem like a distant dream, but it’s never too early to start planning for it. Withdrawals from your 403(b) before age 59½ may trigger income tax and a 10% penalty. But hey, there are exceptions to every rule. If you need to tap into your savings before retirement, you can do so without penalty if you’re using the funds for certain qualified expenses, such as medical bills or a down payment on a home.

Employer Matching

Consider this: your employer could be your secret savings sidekick! Many employers offer matching contributions to their employees’ 403(b) plans. It’s like free money falling into your retirement fund. So, if your employer offers a matching program, don’t pass it up. It’s a fantastic opportunity to boost your savings and secure a brighter financial future.

403(b) Retirement Plan

The 403(b) retirement plan is a tax-advantaged retirement savings vehicle offered to individuals who work for public schools, 403(b) retirement plans function similarly to 401(k) plans which are available to private sector employees. Contributions to a 403(b) plan are made on a pre-tax basis. It reduces your current taxable income, meaning you pay less in taxes now. The money in your 403(b) account grows tax-deferred until you withdraw it in retirement.

Funding Sources

Contributions to a 403(b) plan are made on a pre-tax basis, which reduces your current taxable income. The money in your 403(b) account grows tax-deferred until you withdraw it in retirement, at which time taxes are due. Employers may also make matching contributions to your 403(b) plan, which can further boost your retirement savings.

Investment Options

403(b) plans offer a variety of investment options, including mutual funds, stocks, bonds, and money market accounts. You can choose the investments that meet your risk tolerance and investment goals. It’s important to diversify your investments to reduce your risk.

Eligibility

403(b) plans are available to employees of public schools, colleges, and other tax-exempt organizations. You must meet certain eligibility requirements, such as being employed by an eligible organization and meeting the plan’s age and service requirements.

Withdrawal Options

- Withdrawals from a 403(b) plan are generally subject to taxes and early withdrawal penalties before age 59½. Withdrawals prior to age 59 ½ are penalized at 10%, including any earnings generated by the account.

- Withdrawing earnings

In brief, money earned in your account is taxed as income at your current income tax rate. If your account earned $10,000, you have to pay ordinary income tax on the $10,000 as if you earned it as part of your salary.

- Withdrawing contributions

Unlike earnings, contributions are taxed at your income tax rate at the time you withdraw them. Hence, if your income tax rate is currently 24%, you will only have to pay 24% tax on your contributions.

- Roth Accounts

If you have a Roth 403(b), you will not owe any income tax on your withdrawals in retirement. Roth contributions are taxed when you make them, so you do not pay any tax on withdrawals later on. Remember, you will still have to pay taxes on any earnings in your Roth account.

- Qualified Emergency Distributions

In the event of an especially urgent need, you may withdraw money from your 403(b) accounts without paying the 10% penalty. These qualified emergency distributions are taxed as income, but you may avoid the 10% penalty. You can make qualified emergency withdrawals for the following reasons:

-

To prevent foreclosure or eviction from your primary residence.

-

To pay for unreimbursed medical expenses

-

To pay for qualified higher education expenses

-

To pay for certain funeral expenses

-

Total and Permanent Disability

If you are unable to work due to a disability, you may qualify for a withdrawal from your 403(b) plan without the 10% premature withdrawal penalty. In order to qualify, you must be unable to do any gainful activity for a period expected to be longer than one year or that will result in death.

403(b) Retirement Plan

A 403(b) retirement plan, also known as a tax-sheltered annuity (TSA), is a retirement savings plan available to employees of public schools and certain other tax-exempt organizations. Like 401(k) plans, 403(b) plans allow employees to contribute pre-tax dollars to an investment account, which grows tax-deferred until retirement.

Advantages and Disadvantages

403(b) plans offer potential tax savings and retirement income, but they also come with certain limitations.

Advantages

Tax-deferred growth: Contributions to a 403(b) plan are made with pre-tax dollars, reducing your current taxable income. The money in your account then grows tax-deferred until you withdraw it in retirement.

Employer contributions: Many employers match employee contributions to 403(b) plans, which can add up to free money for retirement.

No income limits: Unlike IRAs and Roth IRAs, there are no income limits for contributing to a 403(b) plan.

Disadvantages

Contribution limits: The annual contribution limit for 403(b) plans is lower than that for 401(k) plans. In 2023, you can contribute up to $20,500 to a 403(b) plan ($26,000 if you’re age 50 or older).

Early withdrawal penalties: If you withdraw money from a 403(b) plan before reaching age 59½, you’ll pay a 10% early withdrawal penalty in addition to income taxes.

Investment options: The investment options available in 403(b) plans are often limited compared to 401(k) plans.

Other Considerations

Roth 403(b) plans: Some employers offer Roth 403(b) plans, which have different tax rules than traditional 403(b) plans. With a Roth 403(b) plan, you contribute after-tax dollars, but your withdrawals in retirement are tax-free.

Employer vesting: Your employer may have vesting requirements for its 403(b) plan. This means that you may not be able to access all of your employer contributions immediately.

Loan provisions: Some 403(b) plans allow employees to take out loans from their accounts. However, these loans must be repaid with interest, and failure to do so can result in early withdrawal penalties.

What is a 403(b) Retirement Plan?

The 403(b) retirement plan is an employer-sponsored retirement savings plan designed specifically for public school employees, certain other tax-exempt organizations, and employees of churches and religious organizations—essentially, anyone who works in the public sector. Like a 401(k) plan, a 403(b) allows employees to make pre-tax contributions to their retirement. This means that the money contributed to the plan is not subject to current income tax, which can result in significant tax savings. In addition, many employers offer matching contributions, which can further boost an employee’s retirement savings.

Benefits of a 403(b) Retirement Plan

403(b) retirement plans offer several important benefits. In addition to the tax advantages mentioned above, 403(b) plans also offer:

- Employer contributions: Many employers offer matching contributions to their employees’ 403(b) plans. This can significantly boost an employee’s retirement savings.

- Investment options: 403(b) plans offer a variety of investment options to choose from, so you can customize your plan to fit your individual investment goals.

- Portability: If you leave your job, you can roll over your 403(b) account to another 403(b) plan or to an IRA. This allows you to keep your retirement savings on track, even if you change jobs.

- Low fees: 403(b) plans typically have lower fees than 401(k) plans, which can save you money in the long run.

Limitations of a 403(b) Retirement Plan

There are also some important limitations to consider before opening a 403(b) retirement plan:

- Contribution limits: The annual contribution limit for 403(b) plans is lower than for 401(k) plans.

- Investment options: 403(b) plans often have a more limited selection of investment options than 401(k) plans.

- Access to funds: Withdrawals from 403(b) plans are subject to a 10% early withdrawal penalty if you take them before age 59½.

How to Open a 403(b) Plan

Individuals eligible for a 403(b) plan can open an account through their employer or a financial institution. If you open an account through your employer, your employer will provide you with the necessary paperwork to complete. If you open an account through a financial institution, you will need to provide the institution with your personal and employment information.

Choosing Investments for Your 403(b) Plan

Once you have opened a 403(b) plan, you will need to choose investments for your account. You should consider your investment goals, risk tolerance, and time horizon. If you are not sure how to choose investments, you can seek advice from a financial advisor.

Managing Your 403(b) Plan

Once you have chosen investments for your 403(b) plan, you will need to manage your account to ensure that it is on track to meet your retirement goals. You should regularly review your investments and make changes as needed.

**403(b) Retirement Plan: A Comprehensive Guide for Employees**

A 403(b) retirement plan, much like the widely recognized 401(k) plan, offers a tax-advantaged way for employees to save for their golden years. However, understanding the intricacies of a 403(b) plan can be daunting, making it essential to delve into its details to maximize its potential.

Eligibility and Contributions

403(b) plans are exclusively available to employees of public schools and certain tax-exempt organizations. Contributions to the plan are made through salary reduction, meaning they are deducted from your paycheck before taxes. Both employees and employers can contribute to the plan, with employee contributions being limited to a specific percentage of their compensation, while employer contributions are subject to annual limits.

Investment Options

403(b) plans offer a wide range of investment options, including mutual funds, ETFs, and annuities. Employees can choose investments based on their risk tolerance and retirement goals. It’s worth noting that investment performance is not guaranteed, and participants should carefully consider their investment choices.

Tax Benefits

Contributions to a 403(b) plan are made on a pre-tax basis, which means they reduce your current taxable income. Earnings on these contributions grow tax-free until they are withdrawn in retirement. Distributions from the plan are taxed as ordinary income, but they may be eligible for favorable tax treatment if taken after age 59.5.

Managing a 403(b) Plan

Regularly monitoring and adjusting your 403(b) plan’s investments is essential for maximizing its effectiveness. Here are some key tips to help you manage your plan:

- Set clear retirement goals. Determine how much you need to save for retirement based on your desired lifestyle and expenses.

- Contribute regularly. Aim to contribute the maximum amount you can afford to take advantage of tax savings and grow your retirement nest egg.

- Diversify your investments. Spread your investments across different asset classes, such as stocks, bonds, and cash, to reduce risk.

- Rebalance your portfolio. Periodically adjust your investment allocations to maintain your desired risk and return profile.

- Consider professional advice. A financial advisor can help you create a personalized investment strategy and make informed decisions.

Remember, a 403(b) retirement plan is a powerful tool for securing your financial future. By understanding its features and managing it effectively, you can maximize its benefits and enjoy a comfortable retirement.

403(b) Retirement Plans: A Comprehensive Guide for Public School Employees and Non-Profit Workers

Public school employees and certain non-profit workers have a unique opportunity to save for retirement through 403(b) retirement plans. These plans offer tax-advantaged savings and can supplement other retirement accounts, such as 401(k)s and IRAs.

What is a 403(b) Retirement Plan?

A 403(b) retirement plan is a tax-advantaged retirement savings plan available to employees of public schools and certain tax-exempt organizations. Contributions to a 403(b) plan are made on a pre-tax basis, which reduces your current taxable income. Earnings on your investments grow tax-deferred, and withdrawals in retirement are taxed as ordinary income.

Eligibility for 403(b) Retirement Plans

To be eligible for a 403(b) retirement plan, you must be an employee of a public school or a qualifying tax-exempt organization. Eligible organizations include:

- Public schools

- Colleges and universities

- Hospitals

- Charities

- Museums

- Religious organizations

Contribution Limits for 403(b) Retirement Plans

The contribution limits for 403(b) retirement plans are set by the IRS and are adjusted annually. For 2023, the contribution limit is $22,500 (plus a catch-up contribution limit of $7,500 for individuals age 50 or older).

Employer Contributions to 403(b) Retirement Plans

Your employer may also choose to make contributions to your 403(b) retirement plan. These contributions are not included in your contribution limit, and they can significantly boost your retirement savings.

Types of Investments Available in 403(b) Retirement Plans

403(b) retirement plans offer a wide range of investment options, including:

- Mutual funds

- Stocks

- Bonds

- Annuities

- Real estate

Withdrawals from 403(b) Retirement Plans

Withdrawals from a 403(b) retirement plan are generally taxed as ordinary income. However, there are exceptions for withdrawals made after age 59½, withdrawals made for certain medical expenses, and withdrawals made as part of a qualified Roth distribution.

Taxes on 403(b) Retirement Plans

Contributions to a 403(b) retirement plan are made on a pre-tax basis, which reduces your current taxable income. Earnings on your investments grow tax-deferred, and withdrawals in retirement are taxed as ordinary income. This means that you pay taxes on your 403(b) savings twice: once when you contribute and again when you withdraw. However, the tax savings you receive during your working years can outweigh the taxes you pay in retirement.

Conclusion

403(b) retirement plans can be a valuable tool for public school employees and certain non-profit workers to save for retirement. They offer tax-advantaged savings, flexible investment options, and the potential for employer contributions. If you are eligible for a 403(b) retirement plan, it is worth considering as part of your overall retirement planning strategy.

No responses yet