What is a 457 Retirement Plan?

Are you an employee of a state or local government agency or a non-profit organization? If so, you may be eligible for a special retirement savings plan known as a 457 plan. We’ll explore what a 457 retirement plan is all about, how it works, and its potential benefits.

A 457 retirement plan is a tax-advantaged savings plan designed specifically for employees of state and local governments and certain qualifying tax-exempt organizations. It allows you to set aside a portion of your pre-tax income for retirement, reducing your current taxable income and potentially boosting your savings.

Think of it as a tax-friendly time capsule where you can stash away money for your golden years. Contributions to a 457 plan are made with pre-tax dollars, which means they’re deducted from your paycheck before taxes are calculated. This reduces your taxable income, potentially lowering your tax bill and increasing your take-home pay. The earnings on your investments within the plan also grow tax-deferred, meaning you won’t owe taxes on them until you withdraw the funds in retirement.

457 plans offer a range of investment options, allowing you to tailor your portfolio to match your risk tolerance and retirement goals. You can choose from mutual funds, target-date funds, and other investment vehicles to create a diversified portfolio that meets your needs.

Contribution Limits

The amount you can contribute to a 457 plan varies depending on your age and whether your employer makes matching contributions. In 2023, the contribution limit for 457 plans is $22,500. If you’re age 50 or older, you can make additional catch-up contributions of up to $7,500. Your employer can also make matching contributions, which can further boost your retirement savings.

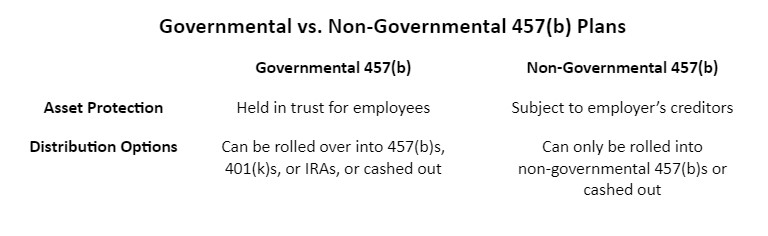

Withdrawal Rules

Withdrawals from a 457 plan are subject to specific rules. Generally, you can withdraw funds from your 457 plan without penalty once you reach age 59½. However, withdrawals made before age 59½ may be subject to a 10% early withdrawal penalty. There are exceptions to this rule, such as withdrawals made for certain qualifying expenses like medical expenses or higher education costs.

Benefits of a 457 Retirement Plan

Participating in a 457 retirement plan offers several potential benefits, including:

- Tax savings: Contributions to a 457 plan are made with pre-tax dollars, reducing your current taxable income and potentially boosting your take-home pay.

- Tax-deferred growth: The earnings on your investments within a 457 plan grow tax-deferred, meaning you won’t owe taxes on them until you withdraw the funds in retirement.

- Investment options: 457 plans offer a range of investment options, allowing you to tailor your portfolio to match your risk tolerance and retirement goals.

- Employer matching contributions: Some employers offer matching contributions to 457 plans, which can further boost your retirement savings.

Conclusion

A 457 retirement plan is a valuable retirement savings option for employees of state and local governments and certain non-profit organizations. It offers tax savings, tax-deferred growth, and a range of investment options. If you’re eligible for a 457 plan, consider taking advantage of this opportunity to save for your future.

What is a 457 Retirement Plan?

Planning for retirement is a crucial aspect of financial security, and there are various retirement plans available to help individuals save for their golden years. One such plan is the 457 retirement plan, a tax-advantaged account offered by state and local governments, as well as certain non-profit organizations. This plan provides a flexible and tax-efficient way to save for retirement, offering benefits that make it a valuable option for eligible individuals and employers alike.

Key Features of a 457 Plan

457 plans come with several key features that make them an attractive retirement planning tool. A key attribute is the tax-deferred growth of investments within the plan. Contributions made to a 457 plan are typically made on a pre-tax basis, which means the funds are deducted from your paycheck before taxes are calculated. This tax savings can add up over time, leading to significant growth in your retirement savings.

Employer contributions are another key feature of 457 plans. Eligible employers can choose to contribute to an employee’s 457 plan, offering a valuable supplement to the individual’s savings. Employer contributions can take the form of matching contributions, whereby the employer matches a certain percentage of the employee’s contributions, or non-matching contributions, where the employer contributes a specific amount regardless of the employee’s contributions.

Additionally, catch-up contributions are available for individuals nearing retirement. Catch-up contributions allow participants to contribute extra funds to their plan up to certain limits. This can be particularly beneficial for individuals who may have started saving for retirement later in their careers or who are seeking to boost their savings before retirement.

457 plans offer flexible investment options, allowing individuals to tailor their investments to suit their risk tolerance and financial goals. Individuals can choose from a range of investment options, including stocks, bonds, mutual funds, and even guaranteed investment contracts. This flexibility gives participants the power to adjust their investments as their needs and circumstances change over time.

Unlike traditional IRAs, there are no income limits to participate in a 457 plan. This makes it an accessible option for individuals at all income levels to save for retirement. The contribution limits for 457 plans are subject to annual adjustments, and individuals should consult with a financial advisor or tax professional to determine the current contribution limits.

Withdrawals from a 457 plan are typically subject to ordinary income tax. However, there are exceptions to this rule, such as withdrawals made after age 59½ or in the event of disability or death. It is important to note that early withdrawals, before age 59½, may be subject to a 10% penalty tax, in addition to ordinary income tax.

Overall, 457 retirement plans offer a wide range of benefits for eligible individuals and employers alike. The tax-advantaged growth, employer contributions, and flexible investment options make 457 plans a valuable tool for retirement planning.

What Is a 457 Retirement Plan?

Wondering what a 457 retirement plan is all about? It’s basically a tax-advantaged savings plan designed specifically for government employees and certain non-profit organizations. Think of it as a retirement nest egg with some unique perks.

You might be thinking, “What’s the big deal?” Well, here’s where it gets interesting: 457 plans let you sock away money for retirement on a tax-deferred basis. That means you pay no income taxes on those contributions right now, potentially saving you a bundle in the long run.

Benefits of a 457 Plan

457 plans don’t just stop at tax deferrals; they come loaded with other advantages too. Let’s dive in:

- Tax-deferred growth: Remember how we talked about contributions being tax-deferred? Well, the investment earnings on those contributions grow tax-free until you retire. It’s like a snowball effect, where your money keeps growing without any tax drag.

- Reduced current taxable income: Contributions to your 457 plan are deducted from your current taxable income. So, you’re not only saving for the future but also potentially lowering your tax bill today.

- Potential employer matching contributions: Many employers offer matching contributions to 457 plans. It’s like free money, so take advantage of it if you can. It’s akin to a supercharger for your retirement savings.

Oh, and did we mention the catch-up provisions? If you’re nearing retirement and haven’t maxed out your 457 contributions, fear not. You can make additional contributions known as “catch-up” contributions, giving you a chance to play catch-up with your retirement savings.

No responses yet