Introduction

Hey there, ever heard of a 403(b) retirement plan? It’s a special savings account that public schools and other non-profit organizations offer to help you save for your golden years — and it comes with some sweet tax advantages.

You might be wondering: what’s the big deal about 403(b) plans? Well, for starters, they’re like little tax shelters. You can contribute money to them on a pre-tax basis, meaning it’s deducted from your paycheck before taxes are calculated. That way, Uncle Sam doesn’t get his grubby little mitts on as much of your hard-earned cash.

But wait, there’s more! When you eventually retire and start taking money out of your 403(b), it’s taxed as ordinary income instead of at your potentially higher current income tax rate. It’s like the taxman is giving you a break for being so darned responsible.

Who’s Eligible for a 403(b) Plan?

So, who’s lucky enough to get their hands on a 403(b) plan? It’s not just for teachers and school administrators. Other public school employees, like bus drivers, cafeteria workers, and even crossing guards, can join the party.

But it doesn’t stop there. Employees of certain tax-exempt organizations, like hospitals, churches, and museums, can also take advantage of these retirement savings accounts.

How Much Can You Contribute to a 403(b) Plan?

Now, let’s talk about the nitty-gritty: how much moolah can you stash away in your 403(b)? For 2023, you can contribute up to $22,500. If you’re 50 or older, you can squeeze in an extra $7,500 as a catch-up contribution.

But there’s a catch: your employer has the final say on how much you can contribute. They might limit your contributions to a certain percentage of your salary or set a fixed dollar amount.

Types of 403(b) Plans

There are two main types of 403(b) plans: traditional and Roth. Traditional 403(b) plans offer tax-deferred growth, meaning your investments grow tax-free until you retire. Roth 403(b) plans, on the other hand, are funded with after-tax dollars. But here’s the kicker: withdrawals in retirement are tax-free.

Investing Your 403(b) Savings

Now, let’s chat about investing your 403(b) savings. You’ll typically have a range of investment options to choose from, including mutual funds, stocks, and bonds. It’s like having your own financial playground.

But here’s the key: don’t let all those options overwhelm you. Start by thinking about your risk tolerance and investment goals. If you’re a risk-taker, you might want to put more of your money in stocks. If you’re more cautious, bonds might be a better fit.

And remember, a diversified portfolio is your friend. Don’t put all your eggs in one basket. Spread your money across different investments to reduce your risk.

403(b) Retirement Plans: A Comprehensive Guide

When it comes to saving for retirement, a 403(b) plan is a powerful tool that can help you reach your financial goals. These plans are designed specifically for employees of public schools and certain other tax-exempt organizations, providing a range of benefits that can make a significant impact on your retirement savings.

Benefits of 403(b) Plans

One of the primary benefits of 403(b) plans is the potential for tax savings. Contributions to these plans are made on a pre-tax basis, meaning they are deducted from your paycheck before taxes are calculated. This can result in significant savings on your current income taxes, and it can also contribute to long-term growth of your retirement savings. In addition to the tax savings, 403(b) plans also offer a wide range of investment options. This allows you to customize your portfolio to meet your individual investment goals and risk tolerance. You can choose from a variety of options, including stocks, bonds, and mutual funds. This flexibility allows you to tailor your retirement savings to your specific needs and goals. Furthermore, 403(b) plans often offer employer matching contributions. This means that your employer may contribute money to your plan on your behalf, up to a certain limit. These matching contributions can give your retirement savings a significant boost, and they can be a valuable way to increase your long-term savings.

Another key benefit of 403(b) plans is the potential for tax-deferred growth. The earnings on your investments in a 403(b) plan are allowed to grow tax-deferred, meaning you won’t have to pay taxes on them until you withdraw the money in retirement. This can result in significant long-term growth of your retirement savings, and it can help you reach your financial goals more quickly. Did you know that 403(b) plans are a great way to save for retirement? They offer a number of benefits, including tax-deferred growth and employer matching contributions. If you’re not already contributing to a 403(b) plan, you should consider doing so today.

403(b) Retirement Plan: A Comprehensive Guide

A 403(b) retirement plan is a tax-advantaged savings account designed specifically for employees of public schools and certain other tax-exempt organizations. This plan offers a range of benefits, including tax-deferred growth, reduced current income taxes, and the potential for tax-free distributions in retirement. If you’re eligible for a 403(b) plan, it can be a valuable tool for securing your financial future.

Contribution Limits

The amount of money you can contribute to your 403(b) plan is subject to annual limits set by the IRS. For 2023, the annual contribution limit is $22,500. If you’re age 50 or older, you’re eligible for an additional catch-up contribution of $7,500, bringing your total contribution limit to $30,000.

Additional Contributions

In some cases, your employer may make additional contributions to your 403(b) plan. These contributions are known as employer matching contributions and are not subject to the annual contribution limits. However, your employer may set limits on the amount of matching contributions they’re willing to make. If you’re fortunate enough to have an employer that offers matching contributions, it’s wise to take advantage of this benefit as much as possible.

Benefits of a 403(b) Plan

There are several key benefits to participating in a 403(b) retirement plan. These benefits include:

- Tax-deferred growth: Contributions to a 403(b) plan are made on a pre-tax basis, which means they reduce your current income taxes. Your investments then grow tax-deferred, meaning you don’t pay taxes on the earnings until you withdraw them in retirement.

- Reduced current income taxes: By reducing your current income taxes, contributions to a 403(b) plan can give you more money to spend or invest today.

- Tax-free distributions in retirement: If you withdraw your 403(b) funds after age 59 1/2, you won’t have to pay any federal income taxes on the withdrawals. This can provide you with a significant tax break in retirement.

- Employer matching contributions: As mentioned earlier, some employers offer matching contributions to their employees’ 403(b) plans. This is a great way to boost your retirement savings without having to contribute more of your own money.

If you’re employed by a public school or other tax-exempt organization, a 403(b) retirement plan can be a valuable tool for securing your financial future. By taking advantage of the tax-advantaged savings and investment opportunities it offers, you can build a comfortable retirement nest egg while reducing your current income taxes.

**403(b) Retirement Plans: A Comprehensive Guide for Educators**

Like a diligent ant preparing for the cold winter, it’s crucial for educators to secure their financial future with a solid retirement plan. Among the various options available, the 403(b) plan stands out as an excellent choice tailored specifically for those employed in public education and certain nonprofit organizations.

**Defining the 403(b) Plan**

A 403(b) plan is a tax-advantaged retirement savings account that allows individuals to contribute pre-tax dollars, reducing their current taxable income. Contributions grow tax-deferred until withdrawal, significantly boosting potential savings over time. Like a snowball rolling downhill, the power of compounding interest can work wonders for your nest egg.

**Eligibility and Contributions**

To be eligible for a 403(b) plan, you must be employed by a public school, college, or other tax-exempt organization. Annual contribution limits vary depending on your age and income, ensuring fairness and flexibility. Employers may also make matching contributions, further enhancing your retirement savings.

**Investment Options**

403(b) plans offer a diversified range of investment options, including mutual funds, stocks, bonds, and exchange-traded funds (ETFs). This buffet-style menu allows you to tailor your investments to your risk tolerance, time horizon, and financial goals.

* **Mutual Funds:** These professionally managed funds provide instant diversification with a single investment, spreading your risk across multiple underlying assets.

* **Stocks:** For those seeking higher growth potential, stocks represent ownership stakes in individual companies, offering the chance to reap the rewards of their success.

* **Bonds:** Bonds are less risky than stocks but offer lower returns. They provide a steady stream of income and can act as a ballast in your investment portfolio during market downturns.

* **ETFs:** ETFs are a hybrid investment that tracks a specific index or basket of assets. They offer instant diversification, low costs, and the flexibility of stock trading.

**Additional Benefits and Considerations**

Beyond tax advantages and investment options, 403(b) plans offer a host of additional benefits to educators:

* **Tax-free withdrawals in retirement:** When you retire, qualified withdrawals from your 403(b) plan are tax-free, helping you preserve your hard-earned savings.

* **Loan provision:** 403(b) plans may allow you to take a loan from your account for financial emergencies or major expenses. However, it’s important to use this feature cautiously and repay the loan in a timely manner.

* **Portability:** When you change jobs within the education sector, you can roll over your 403(b) assets into a similar plan at your new employer, ensuring continuity in your retirement savings.

By embracing the benefits of a 403(b) retirement plan, educators can sow the seeds of a secure and comfortable financial future. It’s like planting an oak tree that will provide shade and shelter for years to come. Don’t let your golden years be overshadowed by financial anxiety. Start saving today with a 403(b) plan and reap the rewards tomorrow!

403(b) Retirement Plans: A Retirement Planning Powerhouse

Nestled within the world of retirement savings options, 403(b) plans shine as a valuable tool for educators and nonprofit employees. These employer-sponsored retirement plans offer a tax-advantaged way to save for your golden years, providing a roadmap to financial security down the road. Ready to dive into the intricacies of 403(b) plans? Let’s take a closer look.

Investment Options Galore

Variety is the spice of life, and 403(b) plans deliver just that when it comes to investment options. With a smorgasbord of choices ranging from mutual funds to annuities, you’re sure to find an investment mix that suits your risk tolerance and financial goals. The freedom to customize your portfolio empowers you to tailor your savings strategy to your unique needs.

Contributions That Stack Up

403(b) plans come with generous contribution limits, giving you ample opportunity to stash away a substantial nest egg. In 2023, you can contribute up to $22,500, or $30,000 if you’re aged 50 or older. Not only that, but your employer may also kick in some extra cash through matching contributions, further bolstering your retirement savings.

Tax Benefits: A Double Whammy

The tax advantages of 403(b) plans are hard to resist. Contributions are made on a pre-tax basis, reducing your current taxable income. And when you retire and start taking withdrawals, those distributions are taxed as ordinary income, potentially at a lower rate than during your working years. It’s like getting a tax break twice, both now and in the future.

Vesting and Withdrawals: Understanding the Fine Print

Contributions made by your employer may be subject to vesting schedules, determining the percentage of funds that are immediately available for withdrawal. Vesting schedules vary from plan to plan, so it’s crucial to understand the rules of your specific plan to avoid any surprises down the road. Withdrawals from 403(b) plans before age 59½ may incur a 10% early withdrawal penalty, so it’s wise to plan your withdrawals carefully.

Comparison to IRAs and 401(k) Plans

403(b) plans share similarities with IRAs and 401(k) plans, but there are some key differences to note. Compared to IRAs, 403(b) plans offer higher contribution limits and access to employer contributions. On the other hand, 401(k) plans tend to have a wider range of investment options and allow for catch-up contributions for those aged 50 or older.

**403(b) Retirement Plans: A Comprehensive Guide**

Retirement planning is a crucial aspect of financial security. One popular option for tax-advantaged savings is the 403(b) retirement plan, commonly available to employees of public schools and certain nonprofit organizations. In this article, we’ll delve into the specifics of 403(b) plans, covering everything you need to know about their benefits, contributions, withdrawals, and tax implications.

**What’s a 403(b) Retirement Plan?**

A 403(b) plan is a retirement savings account specifically designed for employees of public schools and certain tax-exempt organizations. Contributions are deducted from your salary before taxes, reducing your current taxable income. These contributions grow tax-deferred, meaning you won’t owe any taxes on the earnings until you make withdrawals.

**Benefits of 403(b) Plans**

* **Tax-Deferred Growth:** The most significant benefit of a 403(b) plan is its tax advantages. By investing your money pre-tax, you lower your current taxable income and potentially save thousands over the long term.

* **Employer Matching Contributions:** Many employers offer matching contributions to their employees’ 403(b) plans. This is essentially free money that can significantly boost your retirement savings.

* **Employer Contribution Limits:** The IRS sets limits on how much you and your employer can contribute to your 403(b) plan. For 2022, the limit for employee contributions is $20,500 ($27,000 if you’re age 50 or older), and the limit for employer contributions is $61,000 ($67,500 if you’re age 50 or older).

**Contribution Options**

403(b) plans offer two main contribution options:

* **Traditional Contributions:** As mentioned earlier, traditional contributions are deducted from your salary before taxes. You won’t owe any taxes on these contributions or the earnings they generate until you make withdrawals.

* **Roth Contributions:** Roth contributions are made with after-tax dollars. You won’t get an immediate tax deduction, but your qualified withdrawals in retirement will be tax-free.

**Withdrawals from a 403(b) Plan**

When you retire, you can withdraw funds from your 403(b) plan. However, it’s important to be aware of the tax implications:

* **Traditional Contributions:** Withdrawals from traditional 403(b) contributions are taxed as ordinary income. This means you’ll owe taxes on the money you’ve saved, as well as any earnings that have accumulated over the years.

* **Roth Contributions:** Withdrawals from Roth 403(b) contributions are tax-free if you meet certain requirements, including being at least 59½ years old and having had the account for at least five years.

**Taxes on 403(b) Plans**

As mentioned earlier, earnings in a 403(b) plan grow tax-deferred, but withdrawals in retirement are taxed as ordinary income. This means that you’ll owe taxes on the money you’ve saved, as well as any earnings that have accumulated over the years. There are some exceptions to this rule, such as if you make Roth contributions or if you withdraw funds for certain qualified expenses, such as medical expenses or higher education.

It’s crucial to understand the tax implications of 403(b) plans before you invest. Consulting with a financial advisor can help you determine the best savings strategy for your individual circumstances.

**Understanding 403(b) Retirement Plans**

Retirement planning is no walk in the park. But, with the right plan, you can secure your golden years. 403(b) retirement plans, specifically designed for employees of public schools and certain non-profit organizations, offer numerous benefits. Let’s delve into this retirement savings vehicle and explore how it can help you build a nest egg for your future.

**What’s a 403(b) Retirement Plan?**

A 403(b) retirement plan is an employer-sponsored retirement savings plan similar to a 401(k) plan. It allows you to set aside a portion of your salary on a pre-tax basis, reducing your current taxable income. These contributions grow tax-deferred until you retire and begin taking withdrawals.

**Types of 403(b) Plans**

There are two main types of 403(b) plans:

* **Traditional 403(b) Plans:** Contributions are made on a pre-tax basis, reducing your current taxable income. Withdrawals in retirement are taxed as ordinary income.

* **Roth 403(b) Plans:** Contributions are made with after-tax dollars. However, withdrawals in retirement are tax-free. This plan is an excellent option if you expect to be in a higher tax bracket during retirement.

**Advantages of 403(b) Plans**

* **Tax-Deferred Growth:** Contributions grow tax-deferred, meaning you pay taxes on your earnings later in life, potentially when you’re in a lower tax bracket.

* **Employer Contributions:** Many employers offer matching contributions, giving you a free boost to your savings.

* **Portability:** You can roll over your 403(b) balance to an IRA or another 403(b) plan if you leave your job.

**Contribution Limits**

The IRS sets annual contribution limits for 403(b) plans. For 2023, the contribution limit is $22,500 (plus a $7,500 catch-up contribution for those aged 50 or older).

**Eligibility**

403(b) plans are available to employees of public schools and certain tax-exempt organizations. If you’re unsure whether you’re eligible, ask your employer or a financial advisor.

**Benefits of 403(b) Plans and How They Stack Up Against Other Retirement Savings Options**

403(b) plans offer several advantages over other retirement savings options. Compared to traditional IRAs, they have higher contribution limits and allow employer matching contributions. Unlike Roth IRAs, 403(b) plans have no income limits for contributions.

403(b) Retirement Plan: A Comprehensive Guide

Are you an employee of a public school, a hospital, or a 501(c)(3) organization? If so, you may be eligible for a 403(b) retirement plan, a tax-advantaged savings tool designed specifically for employees of these organizations.

In this article, we’ll dive into the world of 403(b) plans, exploring their benefits, contribution limits, investment options, and how they compare to other retirement savings vehicles like 401(k) plans.

Contribution Limits

403(b) plans have lower contribution limits than 401(k) plans, but they still offer a substantial opportunity for tax-deferred savings. For 2023, the annual contribution limit for 403(b) plans is $22,500 ($30,000 if age 50 or older).

Additionally, employers may choose to make matching contributions to their employees’ 403(b) plans, further boosting their retirement savings.

Investment Options

403(b) plans offer a wide range of investment options, including mutual funds, ETFs, and annuities. This flexibility allows you to tailor your investments to your specific risk tolerance and financial goals.

Unlike 401(k) plans, 403(b) plans typically allow you to invest in fixed-rate annuities. These can provide a guaranteed return on your investment, albeit at a lower rate than some other investment options.

Comparison to Other Retirement Plans

403(b) plans have both similarities and differences when compared to 401(k) plans. Both plans offer tax-deferred savings, but 403(b) plans have lower contribution limits. On the other hand, 403(b) plans offer a wider range of investment options, including fixed-rate annuities.

Another key difference is that 403(b) plans are not subject to the same strict regulations as 401(k) plans. This means that 403(b) plans have more flexibility in terms of investment options and plan design.

Tax Benefits

403(b) contributions are made on a pre-tax basis, reducing your current taxable income. Your earnings grow tax-deferred until you withdraw them in retirement, which could be at a lower tax rate.

Depending on your income and filing status, you may also qualify for a Saver’s Credit, which is a tax credit for low- to moderate-income individuals and families who contribute to retirement savings accounts.

Early Withdrawal Penalties

As with most retirement accounts, early withdrawals from a 403(b) plan are generally subject to a 10% early withdrawal penalty. However, there are some exceptions, such as withdrawals for qualified medical expenses or higher education costs.

To avoid the penalty, it’s best to leave your 403(b) savings untouched until you reach retirement age (59.5 years old).

403(b) Retirement Plan: Navigating Your Retirement Savings

Planning for retirement can be a daunting task, but with a 403(b) retirement plan, you can take a proactive approach to securing your financial future. 403(b) plans are retirement savings plans designed for employees of public schools and certain non-profit organizations. Just like 401(k) plans offered by private companies, 403(b) plans allow you to save and invest money on a tax-advantaged basis, helping you grow your savings over time.

Choosing a 403(b) Plan

When you’re ready to choose a 403(b) plan, it’s essential to consider several key factors. First, take a close look at the investment options offered. A diverse range of options, including stocks, bonds, and mutual funds, allows you to customize your portfolio based on your risk tolerance and retirement goals. Additionally, compare the fees associated with different plans. Some plans may charge annual maintenance fees or transaction fees, so it’s essential to factor these costs into your decision.

Employer Contributions

One of the significant benefits of 403(b) plans is the potential for employer contributions. Many employers offer a matching contribution, where they contribute a certain percentage of your salary to your plan. These contributions can significantly boost your savings and help you reach your retirement goals faster.

Tax Advantages

403(b) contributions are made on a pre-tax basis, reducing your current taxable income. This can save you money on your tax bill, especially if you’re in a higher tax bracket. Withdrawals from your 403(b) plan are taxed as income, but the tax savings you accumulate during your working years can offset this.

Investment Options

403(b) plans offer a wide range of investment options, including stocks, bonds, mutual funds, and annuities. This flexibility allows you to tailor your portfolio to your specific investment goals and risk tolerance. Some 403(b) plans may also offer target-date funds, which automatically adjust your asset allocation as you approach retirement.

Fees

When choosing a 403(b) plan, it’s important to consider the fees associated with it. These fees can include annual maintenance fees, transaction fees, and investment management fees. High fees can eat into your investment returns, so it’s essential to compare the fees of different plans before making a decision.

Employer Contributions

Many employers offer matching contributions to their employees’ 403(b) plans. These contributions can significantly boost your retirement savings. For example, if your employer offers a 50% match, your contribution of $1,000 would be matched by an additional $500 from your employer, giving you a total contribution of $1,500 for that year.

Tax Advantages

403(b) plans offer tax advantages that can help you save for retirement. Contributions are made on a pre-tax basis, meaning they are deducted from your income before taxes are calculated. This can result in significant tax savings, especially if you’re in a higher tax bracket. Withdrawals from your 403(b) plan are taxed as income, but the tax savings you accumulate during your working years can offset this.

Investment Options

403(b) plans offer a wide range of investment options to meet your specific financial goals and risk tolerance. These options may include stocks, bonds, mutual funds, and annuities. Some 403(b) plans also offer target-date funds, which automatically adjust your asset allocation as you approach retirement. This can be a convenient option for those who don’t want to actively manage their investments.

Fees

It’s important to consider the fees associated with 403(b) plans. These fees can include annual maintenance fees, transaction fees, and investment management fees. High fees can reduce your investment returns over time, so it’s important to compare the fees of different plans before making a decision. Some 403(b) plans may offer lower fees for higher contribution amounts, so it’s worth considering increasing your contributions if you can afford it.

Employer Contributions

Many employers offer matching contributions to their employees’ 403(b) plans. These contributions can significantly boost your retirement savings. For example, if your employer offers a 50% match, your contribution of $1,000 would be matched by an additional $500 from your employer, giving you a total contribution of $1,500 for that year. If your employer doesn’t offer a matching contribution, you can still benefit from the other tax advantages and investment options that 403(b) plans offer.

What Is a 403(b) Retirement Plan?

A 403(b) retirement plan is a tax-advantaged retirement savings plan for employees of public schools and certain non-profit organizations. Contributions to a 403(b) plan are made on a pre-tax basis, meaning that they are deducted from your paycheck before taxes are calculated. This reduces your current income, which can save you a significant amount of money on taxes. Earnings on your 403(b) investments grow tax-deferred. This means that you don’t pay taxes on the earnings until you withdraw them in retirement. withdraw them in retirement.

Advantages of a 403(b) Retirement Plan

There are many advantages to saving for retirement with a 403(b) plan. Some of the benefits include:

Contribution Limits

The annual contribution limit for a 403(b) plan is $22,500 in 2023 ($30,000 for those age 50 or older). In addition, you may be able to make catch-up contributions if you are behind on your retirement savings. The catch-up contribution limit for 2023 is $7,500.

How to Invest in a 403(b) Retirement Plan

If you are eligible for a 403(b) retirement plan, you can invest by contacting your employer’s human resources department. They will provide you with the necessary paperwork and instructions. Once you have enrolled in the plan, you can choose how much you want to contribute each year and select your investment options.

When to Withdraw From a 403(b) Retirement Plan

You can begin withdrawing money from your 403(b) retirement plan when you reach age 59½. Withdrawals before age 59½ are subject to a 10% early withdrawal penalty. You must begin taking required minimum distributions (RMDs) from your 403(b) plan once you reach age 72. RMDs are the minimum amount of money that you must withdraw from your plan each year. If you fail to take the required minimum distributions, you may be subject to a penalty.

Taxes on 403(b) Withdrawals

When you withdraw money from your 403(b) retirement plan, the withdrawals are taxed as ordinary income. This means that you will pay the same amount of taxes on the withdrawals as you would on your other income.

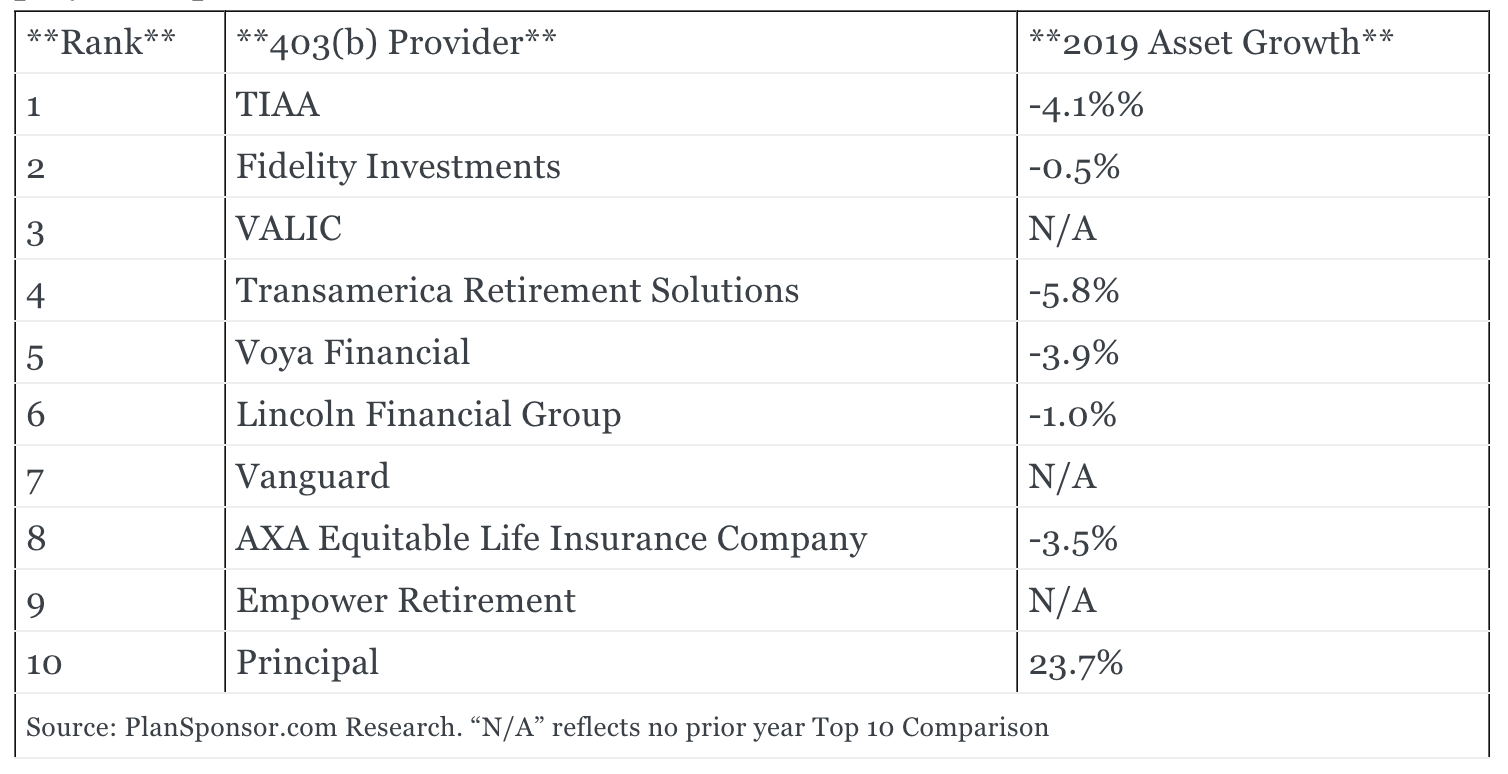

Choosing a 403(b) Retirement Plan Provider

When choosing a 403(b) retirement plan provider, you should consider the following factors:

Conclusion

403(b) retirement plans are a valuable savings tool for employees of public schools and non-profit organizations, offering tax advantages and investment options. If you are eligible for a 403(b) plan, you should consider taking advantage of it. It is a great way to save for retirement and reduce your tax burden.

No responses yet