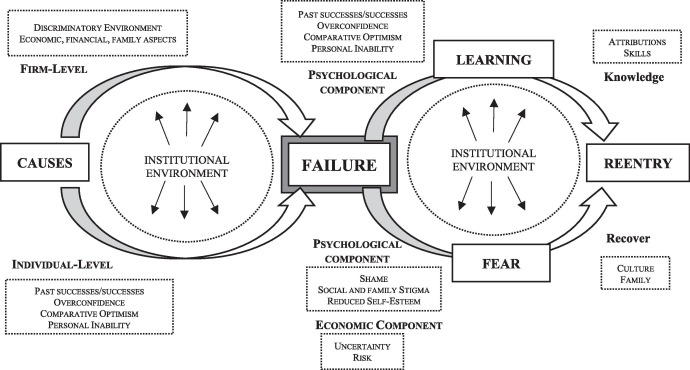

Financial Mistakes in Entrepreneurship

Mistakes are just another word for lessons in the world of entrepreneurship, especially when it comes to the financial side of things. Making smart financial decisions is critical for any business’s success, but it can be especially challenging for entrepreneurs who are often juggling multiple responsibilities and may not have a strong background in finance.

That’s why it’s so important for entrepreneurs to be aware of the common financial mistakes that can derail their businesses. Here are a few to watch out for:

Not Having a Solid Financial Plan

A financial plan is a roadmap for your business’s financial future. It should outline your financial goals, strategies, and how you plan to achieve them. Without a solid financial plan, you’re flying blind and increasing your chances of making costly mistakes.

There are many different ways to create a financial plan. You can do it yourself using a template or software, or you can hire a financial advisor to help you.

Your financial plan should include the following:

- A description of your business and its financial goals

- A breakdown of your income and expenses

- A plan for how you will finance your business

- A strategy for managing your cash flow

- A plan for how you will track your financial progress

Regularly reviewing and updating your financial plan is just as important as creating one in the first place. This will help you stay on track and make adjustments as needed.

Not Knowing Your Numbers

If you don’t know your business’s financial numbers, you can’t make informed decisions about how to manage your money.

At the very least, you should know your:

- Revenue

- Expenses

- Profit

You should also be able to track your cash flow and understand your financial statements.

There are many different ways to track your financial numbers. You can use a spreadsheet, accounting software, or even a simple notebook. What’s important is that you have a system in place for tracking your numbers and that you’re using it consistently.

Common Financial Blunders That Can Sink Your Entrepreneurial Dreams

Entrepreneurship is often glamorized as a path to wealth and independence, but the reality is that many new businesses fail due to avoidable financial mistakes. Here are a few common pitfalls to watch out for:

Poor Cash Flow Management

Cash flow is the lifeblood of any business, and it’s especially critical for startups that are still trying to find their footing. Entrepreneurs need to be able to manage their cash flow effectively in order to keep their business running. This means understanding how much money is coming in and going out, and making sure that there’s enough cash on hand to cover expenses.

One of the biggest cash flow mistakes that entrepreneurs make is overestimating revenue. It’s easy to get caught up in the excitement of a new business and project unrealistic sales figures. But if your actual revenue falls short of expectations, you could quickly find yourself in a cash crunch.

Another common cash flow mistake is underestimating expenses. Starting a business can be expensive, and there are always unexpected costs that can crop up. If you don’t have a realistic budget in place, you could easily run out of money and be forced to close your doors.

To avoid these cash flow pitfalls, entrepreneurs need to develop a solid financial plan. This plan should include realistic revenue projections and expense estimates. It should also include strategies for managing cash flow, such as setting up a line of credit or negotiating extended payment terms with suppliers.

Not Understanding Your Market

One of the most important things for entrepreneurs to do is to understand their target market. This means knowing who their customers are, what they want, and how to reach them. Without a clear understanding of your market, it’s difficult to develop products or services that people will actually buy.

Entrepreneurs who don’t understand their market often make the mistake of trying to be everything to everyone. This is a recipe for failure. It’s better to focus on a specific niche market and become an expert in that area.

To understand your market, you need to do your research. Talk to potential customers, conduct surveys, and analyze industry data. This information will help you develop a clear picture of your target market and create products or services that meet their needs.

Financial Pitfalls That Can Trip Up Entrepreneurs

When starting a business, entrepreneurs often make financial mistakes that can have long-term consequences. These errors can range from overspending to poor budgeting and can lead to financial ruin. Here are some of the most common financial mistakes entrepreneurs make and how to avoid them.

Overspending

One of the biggest financial mistakes entrepreneurs make is overspending in the early stages of their business. Eager to get their business off the ground, they may spend more money than they have on things like equipment, inventory, and marketing. This can lead to a cash flow crunch and make it difficult to pay bills.

To avoid overspending, entrepreneurs should carefully track their expenses and create a budget. They should also be realistic about how much money they have available and not spend more than they can afford.

Poor Budgeting

Another common financial mistake entrepreneurs make is poor budgeting. Not having a solid budget can make it difficult to track expenses and plan for the future. This can lead to financial problems down the road.

To avoid poor budgeting, entrepreneurs should create a detailed budget that includes all of their income and expenses. They should also review their budget regularly and make adjustments as needed.

Inadequate Cash Flow Management

Another common problem that entrepreneurs face is inadequate cash flow management. Cash flow refers to the movement of money in and out of a business. Without adequate cash flow, a business cannot pay its bills or meet its other financial obligations.

To avoid inadequate cash flow, entrepreneurs should carefully track their cash flow and make sure they have enough money on hand to meet their expenses. They should also be prepared for unexpected events that can affect their cash flow, such as a sudden drop in sales or an increase in expenses.

Inadequate Financial Planning

Many entrepreneurs fail to adequately plan for the future. They may not have a business plan or they may not have considered what will happen if their business fails. This can lead to financial problems down the road.

To avoid inadequate financial planning, entrepreneurs should develop a comprehensive business plan that includes financial projections. They should also make sure they have adequate insurance and have a plan in place for what will happen if their business fails.

Overlooking Taxes

Another common financial mistake entrepreneurs make is overlooking taxes. They may not be aware of all the taxes they are required to pay or they may not pay their taxes on time. This can lead to significant financial penalties.

To avoid overlooking taxes, entrepreneurs should make sure they understand all the taxes they are required to pay and that they have a plan in place for paying them on time. They should also consult with a tax advisor if they have any questions.

The Costly Consequences of Financial Missteps in Entrepreneurship

To succeed in entrepreneurship, one must navigate a treacherous financial landscape. Avoidance of pitfalls is paramount for survival, yet many aspiring business owners find themselves entangled in costly traps. One of the most common, yet damaging mistakes lies in the realm of expense tracking.

Not Tracking Expenses

As the adage goes, “If you can’t measure it, you can’t manage it.” This applies unequivocally to entrepreneurship. Without meticulously tracking expenses, one operates blindly, unable to identify areas of financial vulnerability or opportunities for optimization. It’s like driving without a map – you’ll eventually reach a dead end or, worse, crash and burn.

Ignoring Cash Flow

Cash is the lifeblood of any business. Failure to diligently monitor cash flow can lead to a perpetual state of financial stress. It’s like trying to run a marathon without water. You’ll inevitably exhaust your resources and collapse. By anticipating and managing cash flow effectively, entrepreneurs can avoid the dreaded “feast or famine” cycle.

Overspending

The temptation to overspend is ever-present, especially in the early stages of a business. However, spending money without a clear plan is akin to throwing it down a bottomless pit. Every dollar spent must be justified and aligned with the company’s financial goals. Otherwise, it’s like feeding a bottomless void, consuming resources without producing meaningful returns.

Failing to Seek Professional Help

Entrepreneurship is a complex undertaking, and there’s no shame in seeking professional guidance. Accountants, financial advisors, and business mentors can provide invaluable insights and help entrepreneurs navigate the financial intricacies of running a business. It’s like having a compass in a vast and treacherous wilderness. With their expertise, they can help entrepreneurs avoid costly mistakes and steer their businesses towards financial success.

Entrepreneurship is a thrilling adventure filled with potential rewards, but it also comes with its fair share of pitfalls. Financial missteps are among the most common obstacles that can trip up even the most promising ventures. To help you navigate these treacherous waters, we’ve compiled a comprehensive guide to the most common financial mistakes in entrepreneurship, along with tips on how to avoid them.

Not Having a Budget

A budget is the cornerstone of any successful business. It provides a roadmap for your spending, helping you stay on track and avoid overspending. Without a budget, it’s easy to let expenses spiral out of control, leading to financial disaster. Entrepreneurs who fail to create a budget are like sailors setting sail without a compass – they’re destined to drift off course and eventually run aground.

Underestimating Expenses

It’s tempting to underestimate expenses when starting a business, especially if you’re operating on a shoestring budget. However, this can be a costly mistake. When you underestimate expenses, you may find yourself short on cash when bills come due. This can lead to late payments, penalties, and even damage to your credit rating. To avoid this pitfall, be realistic about your expenses and err on the side of caution.

Not Tracking Income and Expenses

Tracking your income and expenses is crucial for understanding the financial health of your business. Without this information, you won’t know where your money is going or whether you’re making a profit. Regularly monitoring your income and expenses will help you identify areas where you can cut costs or increase revenue.

Not Managing Cash Flow

Cash flow is the lifeblood of any business. It’s the money that comes in and out of your business on a daily basis. Managing cash flow is essential for ensuring that you have enough money to cover your expenses and invest in growth. Poor cash flow management can lead to late payments to suppliers, missed opportunities, and even bankruptcy. To avoid this, track your cash flow closely and develop strategies to minimize fluctuations.

Ignoring Financial Advice

Entrepreneurs can often be so focused on their vision and passion that they ignore the importance of financial advice. This can be a big mistake. A qualified financial advisor can provide valuable guidance on everything from budgeting to investing. They can help you make informed decisions that can save you time, money, and stress in the long run. Just as a doctor can help you maintain your physical health, a financial advisor can help you maintain your financial well-being.

Financial Blunders that Can Bury Your Business

Entrepreneurship is a rollercoaster ride filled with exhilarating highs and heart-stopping lows. One of the biggest challenges entrepreneurs face is avoiding the financial pitfalls that can derail their dreams. Let’s dive into some of the most common mistakes that can lead to financial ruin.

Taking on Too Much Debt

Debt can be a double-edged sword. It can provide the necessary capital to grow your business, but if you take on too much, it can suffocate your cash flow and leave you vulnerable to economic downturns. Before taking on any debt, carefully consider your repayment abilities and whether the potential return is worth the risk.

Imagine taking on a massive loan to purchase a new machine. The machine is impressive, but it comes with hefty monthly payments. As the economy takes a downturn, your sales dwindle, leaving you struggling to make the payments. Before you know it, the machine that was supposed to boost your business is now a liability, weighing you down and threatening your survival.

It’s crucial to remember that debt is not free money; it has to be repaid with interest. Before signing on the dotted line, make sure you fully understand the terms and conditions of the loan. Don’t let debt become a millstone around your business’s neck.

Consider seeking guidance from a financial advisor or mentor who can help you navigate the complexities of debt. Remember, a well-managed business is a debt-free business. So, avoid taking on more debt than you can handle and keep your financial house in order.

Financial Blunders: Entrepreneur’s Pitfalls

Entrepreneurship, a venture strewn with both triumphs and setbacks, often presents financial challenges that can make or break a business. Inexperience and a lack of financial savvy can lead entrepreneurs down a perilous path, resulting in costly blunders that could have been avoided. Let’s delve into some of these common financial mistakes and explore strategies to steer clear of them.

Not Seeking Professional Advice

Consultants like accountants, lawyers, and financial advisors serve as beacons of wisdom for entrepreneurs, offering valuable guidance to navigate the intricate world of finance. Ignoring their expertise can prove disastrous, leading to oversights and costly missteps. Just as a doctor knows the human body, these professionals possess a deep understanding of financial matters and can help entrepreneurs make informed decisions, mitigate risks, and optimize their financial performance. Seeking their advice is not a sign of weakness but rather a wise investment in the long-term success of the business.

Cash Flow Mismanagement

Cash flow is the lifeblood of any business, and mismanaging it can lead to severe consequences. Failure to track expenses, monitor cash flow, and forecast future cash needs can result in a cash crunch, limiting the ability to meet obligations and hindering growth. Entrepreneurs must pay close attention to the flow of money in and out of the business, implementing robust systems to manage their cash flow effectively. This includes maintaining accurate records, creating cash flow projections, and seeking external financing when necessary.

Inadequate Budgeting

A budget is the roadmap for a business’s financial journey, providing a framework for responsible spending and informed decision-making. Without a proper budget, entrepreneurs may overspend, depleting resources and putting the business at risk. Creating a realistic budget that aligns with the business’s goals is essential. This involves setting clear financial targets, prioritizing expenses, and adhering to the budget with discipline. It’s not about being cheap; it’s about being strategic with the available funds.

Overextending Credit

Credit can be a powerful tool, but it can also be a double-edged sword. Entrepreneurs who overextend credit to customers or suppliers can find themselves in financial hot water. When customers don’t pay or suppliers demand payment for overdue invoices, it can put a strain on the business’s cash flow and damage relationships with key vendors. It’s crucial to establish clear credit policies, conduct thorough credit checks, and monitor accounts receivable and payable closely to avoid credit-related problems.

Mixing Personal and Business Finances

Keeping personal and business finances separate is paramount for both legal and financial reasons. Commingling funds can lead to tax complications, confusion, and potential legal issues. Entrepreneurs should maintain separate bank accounts for their business, ensuring that business expenses and revenues are clearly distinct from personal transactions. This separation helps protect personal assets from business liabilities and enhances the credibility of the business.

Failing to Plan for Growth

All businesses should plan for the future, regardless of their current size or success. Failing to plan for growth can lead to missed opportunities, inadequate resources, and financial challenges as the business expands. Entrepreneurs should develop a long-term vision for their business and devise financial strategies to support that growth. This may involve securing additional funding, investing in new equipment or facilities, and expanding into new markets.

No responses yet