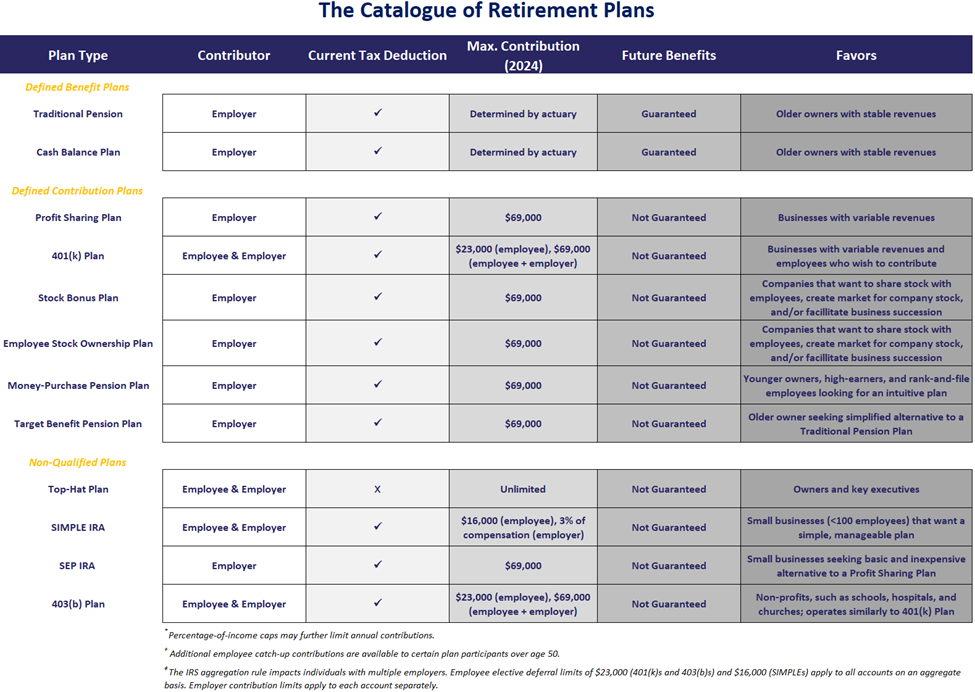

Types of Retirement Plans

When it comes to planning for your golden years, there’s no shortage of options. From 401(k)s to IRAs to annuities, the retirement landscape can seem like a labyrinth. But don’t let the complexity overwhelm you – understanding the different types of retirement plans is the key to making an informed decision about your financial future.

Defined-Contribution Plans

Defined-contribution plans are a popular choice for retirement savings, and for good reason. These plans offer a straightforward approach to retirement investing, with contributions made on a pre-tax basis. With defined-contribution plans, your contributions and any investment earnings grow tax-deferred until you retire.

The most common type of defined-contribution plan is the 401(k), offered by many employers. 401(k) plans allow you to contribute a portion of your paycheck on a pre-tax basis, up to a certain limit set by the IRS. Your employer may also make matching contributions, giving you an extra boost to your retirement savings.

Another popular defined-contribution plan is the Individual Retirement Account (IRA). IRAs are available to anyone with earned income, regardless of employment status. With IRAs, you can make contributions on a pre-tax or after-tax basis, depending on your preference.

Defined-Benefit Plans

Defined-benefit plans are a different type of retirement plan that offers a more predictable retirement income stream. With defined-benefit plans, your retirement benefits are based on a formula that considers factors such as your salary, years of service, and age. This means that you know exactly how much you will receive in retirement, regardless of how the market performs.

Defined-benefit plans are often offered by government agencies, schools, and some large corporations. However, they are becoming increasingly rare in the private sector.

Annuities

Annuities are a type of retirement investment that provides a guaranteed income stream for a specific period of time or for the rest of your life. With annuities, you make a lump sum payment or a series of payments to an insurance company. In return, the insurance company agrees to pay you a regular income for a guaranteed period of time.

Annuities can provide peace of mind in retirement, ensuring that you will have a steady income stream to cover your basic expenses. However, it’s important to note that annuities can be complex and have high fees, so it’s important to do your research before you purchase one.

Which Type of Retirement Plan Is Right for Me?

The best type of retirement plan for you will depend on your individual circumstances and financial goals. Consider your age, income, risk tolerance, and retirement lifestyle when making your decision. It’s also a good idea to consult with a financial advisor to get personalized advice on your retirement planning.

Types of Retirement Plans

Retirement planning is a complex and multifaceted endeavor, but it’s essential for securing your financial future. One of the most important decisions you’ll make in this process is choosing the right type of retirement plan. There are two main types of retirement plans: defined benefit plans and defined contribution plans.

Defined Contribution Plans

Defined contribution plans are tax-advantaged accounts that allow you to contribute a portion of your income on a pre-tax basis. Your investments then grow tax-deferred until you retire. When you withdraw money from the account, you’ll pay taxes on the earnings. There are two main types of defined contribution plans: 401(k)s and IRAs.

401(k) plans are offered by employers and allow you to contribute a portion of your paycheck to a tax-advantaged account. Your employer may also make matching contributions, which can help you save even more. 401(k) plans have contribution limits that vary each year, but you can contribute up to $20,500 in 2023. If you’re 50 or older, you can make catch-up contributions of up to $7,500.

IRAs are individual retirement accounts that you can open on your own. There are two types of IRAs: traditional IRAs and Roth IRAs. Traditional IRAs allow you to contribute pre-tax dollars, and your earnings grow tax-deferred. When you withdraw money from the account, you’ll pay taxes on the earnings. Roth IRAs allow you to contribute after-tax dollars, but your earnings grow tax-free. When you withdraw money from the account, you won’t pay taxes on the earnings.

Defined contribution plans are a good option if you’re looking for a way to save for retirement on your own. They offer tax-advantaged savings and can help you accumulate a significant nest egg over time.

**Types of Retirement Plans**

When it comes to planning for your retirement, it’s never too early to start. One of the most important decisions you’ll make is choosing the right retirement plan. There are a variety of plans available, each with its own unique benefits and drawbacks. In this article, we’ll take a closer look at the different types of retirement plans to help you make an informed decision.

**Defined Benefit Plans**

Defined Benefit Plans

Defined benefit plans, also known as pensions, are employer-sponsored retirement plans that guarantee a specific retirement income based on factors such as your salary and years of service. With a defined benefit plan, you don’t have to worry about investment risk, as the employer assumes all responsibility for managing the plan’s investments and ensuring that there are sufficient funds to pay your retirement benefits. Defined benefit plans are becoming increasingly rare, but if you’re lucky enough to have one, it can provide you with a secure and comfortable retirement.

**Defined Contribution Plans**

Defined Contribution Plans

Defined contribution plans are another type of employer-sponsored retirement plan, but unlike defined benefit plans, they do not guarantee a specific retirement income. Instead, your retirement savings are based on the amount of money you and your employer contribute to the plan, as well as the investment returns you earn on those contributions. There are two main types of defined contribution plans: 401(k) plans and 403(b) plans.

401(k) plans are available to employees of for-profit companies, while 403(b) plans are available to employees of public schools and certain other non-profit organizations. Both types of plans allow you to make pre-tax contributions to your retirement savings, which can reduce your current taxable income.

**IRAs**

IRAs (Individual Retirement Accounts) are retirement savings accounts that are not sponsored by an employer. Anyone can open an IRA, regardless of their employment status. There are two main types of IRAs: traditional IRAs and Roth IRAs.

Traditional IRAs allow you to make tax-deductible contributions to your retirement savings. However, you will have to pay taxes on the money when you withdraw it in retirement. Roth IRAs, on the other hand, allow you to make after-tax contributions to your retirement savings. However, you can withdraw the money tax-free in retirement.

**Choosing the Right Retirement Plan**

The best retirement plan for you will depend on your individual circumstances. Consider your age, income, risk tolerance, and retirement goals when making your decision. If you’re not sure which type of plan is right for you, talk to a financial advisor for help.

Types of Retirement Plans

When the time comes to retire, it’s wise to have a plan in place to ensure you can maintain your current lifestyle. There are multiple types of retirement plans, each with its own set of benefits and drawbacks. Consider the following options to find the one that best suits your needs.

401(k) Plans

401(k) plans are employer-sponsored retirement plans that allow employees to contribute a portion of their paycheck before taxes. This reduces their current taxable income, potentially saving them money. Contributions are invested in a variety of options, such as stocks, bonds, and mutual funds. Some employers match a portion of employee contributions, making them an even more attractive option.

Benefits of 401(k) Plans

- Tax-deferred growth: Earnings on investments are not taxed until withdrawal, potentially allowing for significant long-term growth.

- Employer matching: Many employers match a portion of employee contributions, essentially providing free money.

- Variety of investment options: Participants can choose from a wide range of investment options to align with their risk tolerance and retirement goals.

Drawbacks of 401(k) Plans

- Contribution limits: There are annual limits on how much individuals can contribute to their 401(k) plans.

- Early withdrawal penalties: Withdrawing money from a 401(k) plan before age 59½ may result in penalties and taxes.

- Investment risk: Investments in 401(k) plans are subject to market fluctuations, potentially leading to losses.

Types of Retirement Plans

Planning for retirement can be a daunting task, but it’s essential to secure your financial future. With various retirement plans available, it’s crucial to understand the different options to determine the best fit for your needs. Here’s an in-depth look at the main types of retirement plans.

IRAs

IRAs are individual retirement accounts that enable individuals to save for retirement tax-advantaged, regardless of their employment status. IRAs offer two primary options: Traditional IRAs and Roth IRAs. Traditional IRAs allow you to deduct contributions from your taxable income, while Roth IRAs feature tax-free withdrawals in retirement.

401(k) Plans

401(k) plans are employer-sponsored retirement plans that allow employees to contribute pre-tax dollars from their paychecks. Contributions are invested in mutual funds, stocks, or other investment options. Employers may also make matching contributions, further bolstering retirement savings.

403(b) Plans

403(b) plans are similar to 401(k) plans, but they’re designed for employees of public schools and certain other tax-exempt organizations. Contributions are also made on a pre-tax basis, and earnings grow tax-deferred until withdrawals are made in retirement.

Defined Benefit Pension Plans

Defined benefit pension plans are employer-sponsored plans that promise to pay a specific monthly benefit in retirement based on factors such as years of service and salary. These plans are less common than they once were, but they still provide a guaranteed income stream in retirement.

Annuities

Annuities are insurance contracts thatguarantee a steady stream of income for a specific period or the rest of your life. You can purchase annuities with a lump sum or through regular payments. Annuities can help ensure a secure retirement income, but they may have high fees and surrender charges.

**Types of Retirement Plans: Navigating the Maze to a Secure Future**

Retirement may seem like a distant dream, but planning for it is crucial to ensure a comfortable golden age. The bewildering array of retirement plans can be daunting, but understanding their intricacies will empower you to make informed decisions that can secure your financial well-being.

**Traditional IRA and 401(k): Tax-Deferred Savings**

Traditional Individual Retirement Accounts (IRAs) and 401(k) plans offer tax-deferred savings, meaning contributions are made pre-tax, reducing your current income. However, withdrawals in retirement are taxed as ordinary income. This strategy is ideal for those expecting to be in a lower tax bracket during retirement.

**Roth IRA and 401(k): Tax-Free Withdrawals**

Roth IRAs and 401(k) plans, on the other hand, offer tax-free withdrawals in retirement. Contributions are made post-tax, but earnings grow tax-free, and withdrawals are untaxed. This approach benefits those who anticipate being in a higher tax bracket in retirement.

Traditional vs. Roth Accounts

Deciding between traditional and Roth accounts depends on several factors:

* **Current income and tax bracket:** If you’re in a high tax bracket now, a traditional account may be more beneficial. Conversely, if you expect to be in a higher bracket during retirement, Roth accounts might be more suitable.

* **Expected retirement income:** If you anticipate having a high retirement income, Roth accounts can be more advantageous as tax-free withdrawals won’t increase your overall tax burden.

* **Risk tolerance:** Traditional accounts offer a more predictable return, while Roth accounts carry more investment risk but potentially higher rewards.

* **Investment horizon:** If you have a long investment horizon, Roth accounts benefit from tax-free compounding over time. For shorter horizons, traditional accounts may be more appropriate.

Employer-Sponsored Plans

Many employers offer employer-sponsored retirement plans, such as 401(k)s and 403(b)s. These plans often provide matching contributions, essentially free money that boosts your savings.

**Annuities: Guaranteed Income for Life**

Annuities provide guaranteed income for life. You make contributions and select an income stream that will begin at retirement. This can provide peace of mind and protect against outliving your savings.

**Other Retirement Savings Options**

In addition to these major plans, consider other retirement savings options such as Health Savings Accounts (HSAs) and non-qualified annuities. Understanding the nuances of each can help you create a customized retirement plan that aligns with your needs and goals.

**What Are the Different Types of Retirement Plans?**

Retirement plans come in all shapes and sizes, from 401(k)s to IRAs to annuities. Choosing the right one for you is an important decision, as it will affect your financial security in your later years. Here’s a quick overview of the most common types of retirement plans:

401(k) Plans

401(k) plans are employer-sponsored retirement plans that allow employees to save for retirement on a pre-tax basis. This means that you contribute money to your 401(k) account before taxes are taken out of your paycheck. This reduces your current taxable income, which can save you money on taxes now. Many employers also match employee contributions to 401(k) plans, which can give your savings a big boost.

Traditional IRAs

Traditional IRAs are individual retirement accounts that allow you to save for retirement on a tax-deferred basis. This means that you don’t pay taxes on your earnings until you withdraw the money in retirement. Traditional IRAs have contribution limits that are lower than 401(k) plans, but they offer more investment options.

Roth IRAs

Roth IRAs are similar to traditional IRAs, but they are funded with after-tax dollars. This means that you don’t get a tax break on your contributions now, but your earnings grow tax-free and you can withdraw them tax-free in retirement. Roth IRAs have income limits that determine who is eligible to contribute to them.

Annuities

Annuities are insurance contracts that provide you with a guaranteed income stream in retirement. You can purchase an annuity with a lump sum or with a series of payments. Annuities can be a good option for people who want to ensure that they will have a steady income in retirement, but they can be expensive and they may not be suitable for everyone.

Choosing the Right Retirement Plan

The best retirement plan for you depends on your individual circumstances and financial goals. Consider factors such as your income, age, and risk tolerance. If you’re not sure which type of retirement plan is right for you, talk to a financial advisor

No responses yet