Introduction

Personal finance mistakes are lurking everywhere, waiting to trip us up and derail our financial futures. From impulsive purchases to ill-conceived investments, these pitfalls can cost us dearly. To safeguard our financial well-being, it’s crucial to steer clear of these common traps. Here’s a comprehensive guide to the worst financial mistakes and how to avoid them.

1. Living Beyond Your Means

Living beyond your means is a surefire recipe for financial disaster. When you spend more than you earn, you’re digging yourself into a pit of debt. The interest charges on that debt can quickly snowball, making it harder and harder to get ahead. Like a leaky faucet, your finances will slowly but surely drain away until you’re left with nothing. To avoid this trap, create a budget and stick to it. Track your income and expenses so you know where your money is going. Once you identify areas where you’re overspending, make adjustments to bring your spending in line with your income. It may seem like a small change, but it can make a huge difference in the long run.

For example, let’s say you earn $5,000 a month and your expenses total $5,500. That means you’re overspending by $500 each month. If you can cut back on non-essential expenses, like entertainment or dining out, you can free up that $500 and start saving it instead. Over time, those savings can add up to a significant nest egg.

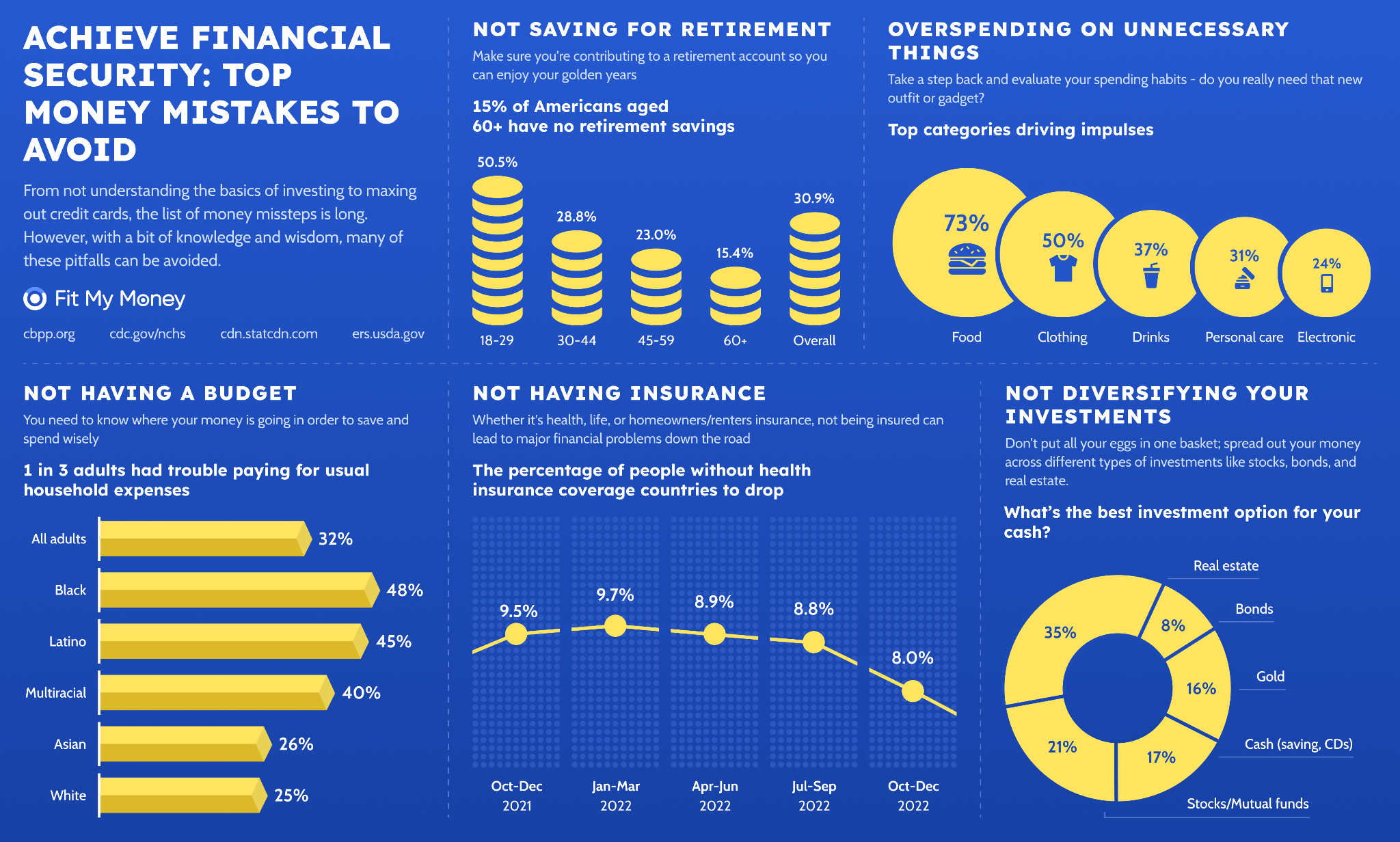

2. Not Saving for Retirement

Retirement may seem like a distant reality, but it’s never too early to start saving. The sooner you start, the more time your money has to grow and compound. If you wait until you’re older to start saving, you’ll need to set aside more money each month to reach your retirement goals. It’s like trying to fill a bucket with a leaky bottom—no matter how much you pour in, it’s going to keep leaking out. Start saving early, even if it’s just a small amount each month. Your future self will thank you for it.

**7 Costly Financial Mistakes to Avoid Like the Plague**

We’ve all made poor financial choices at some point. Maybe we blew our savings on a lavish vacation or splurged on a designer bag we couldn’t afford. Making financial mistakes is normal, but making the same ones over and over again can have severe consequences.

Here are seven of the worst financial mistakes you can make, along with tips on how to avoid them:

Mistake #1: Not Budgeting

A budget is the foundation for financial control and stability. It allows you to track your income and expenses so you can make informed choices about how to spend your money. If you don’t budget, you’re more likely to overspend and get into debt.

How to avoid it: Create a monthly budget that tracks all of your income and expenses. Be realistic about how much you can spend each month, and stick to your budget as much as possible.

Mistake #2: Not Saving for Retirement

Retirement may seem like a distant dream, but it’s never too early to start saving. The sooner you start, the more time your money has to grow. If you wait until you’re in your 50s or 60s to start saving, you’ll need to save a lot more money to reach your retirement goals.

How to avoid it: Start saving for retirement as early as possible. Even if you can only save a small amount each month, it will add up over time.

Not saving for retirement is like trying to drive to California without a map or GPS. You might eventually get there, but it will be a bumpy ride, and you’re likely to get lost along the way.

Mistake #3: Not Investing

Investing is a great way to grow your wealth over time. However, it’s important to invest wisely. Don’t put all of your eggs in one basket, and diversify your investments so you can reduce your risk.

How to avoid it: Educate yourself about investing before you start. There are many resources available to help you learn about different investment options.

Mistake #4: Not Buying Life Insurance

Life insurance is a safety net for your loved ones. If you die, your life insurance policy will provide your family with financial support. It can help them pay for funeral expenses, mortgage payments, and other living expenses.

How to avoid it: Get life insurance as soon as you can afford it. The younger you are, the lower your premiums will be.

Mistake #5: Living Paycheck to Paycheck

Living paycheck to paycheck is a surefire way to get into debt. If you’re constantly spending all of your money, you’ll have nothing left over to save or invest. And if you have an emergency, you’ll be left scrambling to find the money to cover it.

How to avoid it: Create a budget and stick to it. Make sure you’re saving and investing a portion of your income each month.

Mistake #6: Not Setting Financial Goals

If you don’t know what you’re working towards, it’s hard to stay motivated to save and invest. That’s why it’s important to set financial goals. Whether you want to buy a house, retire early, or pay for your child’s education, having a financial goal will help you stay on track.

How to avoid it: Take some time to think about your financial goals and write them down. Once you know what you’re working towards, you can create a plan to achieve your goals.

Mistake #7: Not Getting Help

If you’re struggling to manage your finances, don’t be afraid to get help. There are many resources available to help you get back on track, including financial counselors, credit counselors, and non-profit organizations.

How to avoid it: Don’t wait until you’re in financial trouble to get help. If you’re struggling to manage your finances, reach out to a financial counselor or credit counselor for help.

Worst Financial Mistakes You’re Making Without Realizing It

Money management is a crucial aspect of our lives, yet many of us make financial mistakes that can have severe consequences. These blunders can range from overspending to not saving enough for retirement, and they can lead to debt, financial distress, and even bankruptcy. In this article, we’ll delve into some of the worst financial mistakes you might be making without even realizing it, shedding light on their potential impact and providing guidance on how to avoid them.

Mistake #1: Impulse Buying

Impulse buying is the act of making unplanned purchases without giving careful consideration to their necessity or affordability. This can be triggered by emotions like excitement, boredom, or stress, and it can lead to wasted money and unnecessary debt. For instance, if you find yourself frequently buying things you don’t really need just because they’re on sale, you may be falling into the trap of impulse buying.

Mistake #2: Overspending

Overspending occurs when you spend more money than you earn, which can lead to debt and financial distress. This can be caused by various factors, such as poor budgeting, unrealistic expectations, or a lack of financial discipline. For example, if you consistently spend more than you bring in each month and rely on credit cards to cover the difference, you may be at risk of overspending.

Mistake #3: Not Having an Emergency Fund

An emergency fund is a crucial safety net that can protect you from unforeseen financial emergencies, such as job loss, medical expenses, or home repairs. Without an emergency fund, you may be forced to rely on high-interest debt or borrow money from family and friends to cover unexpected costs. Not having an emergency fund is like driving a car without insurance – it may seem fine until you have an accident and need it the most. Experts recommend setting up an emergency fund that covers at least three to six months’ worth of living expenses.

Mistake #4: Not Saving for Retirement

Retirement may seem like a distant reality, but it’s never too early to start saving. Many people make the mistake of not saving enough for their retirement, which can lead to financial hardship in their later years. The earlier you start saving, the more time your money has to grow through compound interest. Think of it this way: saving for retirement is like planting a tree – the sooner you plant it, the taller and stronger it will grow over time.

Mistake #5: Ignoring Credit Card Debt

Credit cards can be a convenient way to make purchases, but ignoring credit card debt can lead to serious financial consequences. If you only make minimum payments on your credit cards, it can take years to pay them off, and you’ll end up paying a significant amount of interest. Additionally, high credit card debt can damage your credit score, making it harder to qualify for loans or credit in the future. Credit card debt is like a snowball rolling down a hill – if you don’t stop it, it will only get bigger and harder to manage.

Seven Costly Financial Missteps That Could Derail Your Economic Well-being

Making unwise financial decisions can have far-reaching ramifications, potentially jeopardizing our long-term economic well-being. Avoiding these common pitfalls is imperative for safeguarding our financial future. Here’s a comprehensive overview of some of the most debilitating financial blunders to steer clear of:

Mistake #1: Living Beyond Your Means

Falling into the trap of spending more than you earn is a recipe for financial ruin. This can quickly lead to mounting debt and missed payments, causing irreparable damage to your credit score. It’s essential to create a realistic budget and stick to it, ensuring that your expenses don’t exceed your income.

Mistake #2: Not Having an Emergency Fund

Life is full of surprises, and financial emergencies can strike at any moment. Not having an emergency fund in place can leave you vulnerable to unforeseen expenses, forcing you to resort to high-interest loans or dipping into your savings. Aim to save at least three to six months’ worth of living expenses to weather unexpected financial storms.

Mistake #3: Ignoring Retirement Planning

Retirement may seem like a distant concern, but it’s never too early to start planning. Delaying saving for retirement can significantly impact the size of your nest egg down the road. Start contributing to a retirement account as early as possible and maximize your contributions to take advantage of tax-deferred growth.

Mistake #4: Taking on Too Much Debt

Debt can be a useful tool when used wisely, but it can also become a dangerous burden if not managed responsibly. Avoid taking on more debt than you can afford to repay. Consider your income, expenses, and credit score before applying for loans or credit cards. Remember, every dollar you pay in interest is money that could be invested for your future.

Mistake #5: Impulse Purchases

The allure of instant gratification can lead us to make impulsive purchases that we later regret. Before hitting the buy button, ask yourself if you truly need the item and if it fits within your budget. Impulse purchases can quickly derail your financial goals and create unnecessary clutter in your life.

Mistake #6: Not Investing

Investing is a crucial element of building wealth over time. The sooner you start investing, the more time your money has to grow through compound interest. Don’t be afraid to seek professional advice to create a diversified portfolio that aligns with your risk tolerance and financial goals.

Mistake #7: Not Protecting Your Assets

Life insurance, health insurance, and disability insurance are essential safeguards against unexpected events. These policies provide peace of mind and financial protection for you and your loved ones. Review your insurance coverage regularly to ensure that it meets your changing needs.

**Worst Financial Mistakes: A Path to Financial Ruin**

Financial blunders, like potholes on a highway, can derail our financial aspirations. While some mistakes are merely bumps in the road, others can be like sinkholes, leading to financial despair. One such colossal error is taking on excessive debt.

**Mistake #4: Taking on Too Much Debt**

Debt, when used judiciously, can be a powerful tool for building wealth. However, when it spirals out of control, it can become a financial albatross, weighing us down and making it difficult to breathe.

Excessive debt can manifest in various forms: student loans, credit card balances, or mortgages that stretch beyond our means. The allure of instant gratification can blind us to the long-term consequences of borrowing beyond our ability to repay.

The burden of debt can crush our financial well-being. It can consume a significant portion of our income, leaving us with less for essential expenses, savings, and investments. This financial squeeze can make it challenging to keep up with bills, increase our savings, or weather unexpected financial storms.

Moreover, excessive debt can damage our credit scores, making it harder to secure favorable loan terms or even qualify for basic financial services. This domino effect can create a vicious cycle of debt and financial distress.

To avoid this financial quagmire, it’s crucial to exercise caution when taking on debt. Before borrowing, create a realistic budget that accounts for all your expenses, including debt repayments. Only borrow what you need and can afford to repay on time. Additionally, explore alternatives to debt, such as saving or seeking financial assistance from trusted sources.

Worst Financial Mistakes

Everyone makes mistakes, but some can cost you dearly. Especially when it comes to your finances. Avoiding these common financial pitfalls can help you save money, reach your financial goals, and protect your financial well-being.

Mistake #1: Spending More Than You Earn

This is a surefire way to get into debt. If you’re spending more than you earn, you’re digging yourself a financial hole. Make a budget and stick to it. Track your income and expenses, and find ways to cut back on unnecessary spending.

Mistake #2: Not Having an Emergency Fund

Life is unpredictable. A flat tire, a medical emergency, or a job loss can happen at any time. That’s why it’s important to have an emergency fund to cover unexpected expenses. Aim to save up at least three to six months’ worth of living expenses.

Mistake #3: Not Investing

Investing helps grow your money over time and secure your financial well-being. Whether it’s through stocks, bonds, or mutual funds, investing can help you reach your financial goals faster. Don’t put all your eggs in one basket. Diversify your investments to reduce risk.

Mistake #4: Not Planning for Retirement

Retirement may seem like a long way off, but it’s never too early to start planning. The sooner you start saving, the more time your money has to grow. Take advantage of tax-advantaged retirement accounts like 401(k)s and IRAs.

Mistake #5: Not Protecting Your Income

Disability insurance and life insurance are two important ways to protect your income and your family’s financial security. If you’re disabled or pass away, these policies can help replace your lost income and cover expenses.

Mistake #6: Taking on Too Much Debt

Debt can be a financial burden, and too much debt can be overwhelming. If you’re carrying too much debt, it can be difficult to make ends meet and reach your financial goals. Consolidate your debts, negotiate lower interest rates, and develop a plan to pay off your debt as quickly as possible.

Mistake #7: Not Reading the Fine Print

Before you sign any financial agreement, make sure you understand all the terms and conditions. Don’t be afraid to ask questions and get clarification on anything you don’t understand. This will help you avoid unpleasant surprises down the road.

Mistake #8: Not Seeking Professional Advice

If you’re facing financial challenges or have complex financial needs, don’t hesitate to seek professional advice. A financial advisor can help you develop a personalized financial plan that meets your specific needs and goals.

Making a financial mistake is like taking a wrong turn on a road trip – it can lead you down a path of frustration, regret, and potential financial ruin. If you’re not careful, you could end up veering off course and into a ditch. To help you avoid these financial pitfalls, we’ve compiled a list of the worst financial mistakes you can make, along with tips on how to steer clear of them.

Mistake #6: Not Protecting Yourself

When it comes to your finances, it’s always better to be safe than sorry. That’s why it’s crucial to have adequate insurance coverage in place. Insurance acts as a safety net, protecting you from unexpected events that could wipe out your savings or put you in debt. It’s like having a financial airbag that inflates when things go wrong.

In addition to insurance, it’s also essential to have an emergency fund. This is a stash of money that you can tap into when you face unexpected expenses, such as a medical emergency or a job loss. An emergency fund can help you weather financial storms without having to resort to debt. Just like a spare tire in your car, an emergency fund can give you peace of mind knowing that you’re prepared for whatever life throws your way.

Worst Financial Mistakes: Lessons Learned the Hard Way

Money mistakes can happen to anyone, but some are more costly than others. Here are several common financial blunders that can take a significant toll on your financial well-being, along with tips to avoid them.

Mistake #7: Falling for Scams

With the rise of technology, it’s easier than ever for scammers to target unsuspecting individuals online and offline. Remember the adage, “If it sounds too good to be true, it probably is.” Be vigilant about protecting your hard-earned money. Stay informed about common scams and never provide personal or financial information to strangers.

Mistake #8: Impulse Spending

In the age of instant gratification, it’s tempting to succumb to impulse purchases that can quickly derail your financial goals. It’s tempting to give in to impulse purchases, especially when you’re feeling down or stressed. However, it’s important to remember that these purchases often end up being unnecessary and can add up quickly. If you find yourself tempted to make an impulse purchase, take a few minutes to think about whether you really need it. Chances are, you’ll realize that you can live without it. Additionally, consider setting a budget for yourself and sticking to it. This will help you to avoid overspending and make more informed financial decisions.

Impulse spending can be likened to a slippery slope. It starts with small purchases here and there, but before you know it, you’re spending more than you intended. To avoid this, make a conscious effort to be mindful of your spending habits. Keep track of your purchases, even the small ones, and see where your money is going. Once you have a better understanding of your spending patterns, you can start to make changes to reduce impulse spending.

Another way to avoid impulse spending is to give yourself a cooling-off period before making a purchase. When you see something you want, don’t buy it right away. Wait a few days or even weeks to see if you still want it. Chances are, you’ll forget about it or find something else you like better.

Finally, if you find yourself struggling to control your impulse spending, don’t be afraid to seek help. There are many resources available, such as credit counseling and financial planning services, that can help you to get back on track.

Top 9 Worst Financial Mistakes and How to Avoid Them

Mistakes happen. But when it comes to your hard-earned money, there are certain missteps you don’t want to make. From living beyond your means to ignoring retirement savings, these are some of the most common financial blunders people make – and how to avoid them. Trust us, your future self will thank you.

1. Spending More Than You Earn

It’s a classic financial faux pas: spending more money than you make. When you live beyond your means, you’re essentially borrowing from your future self, which can lead to a cycle of debt. To avoid this trap, create a budget and stick to it. Track your income and expenses, and make sure you’re not overspending in any category. If you’re struggling to make ends meet, consider cutting back on non-essential expenses or finding ways to increase your income.

2. Ignoring Retirement Savings

Retirement may seem like a long way off, but it’s never too early to start saving. The sooner you start, the more time your money has to grow. Even if you can only contribute a small amount each month, it will add up over time. Take advantage of employer-sponsored retirement plans, such as 401(k)s or 403(b)s, if they’re available to you. These plans offer tax benefits that can help you save even more.

3. Taking on Too Much Debt

Debt can be a useful tool, but it’s important to use it wisely. Too much debt can quickly become overwhelming, especially if you lose your job or have unexpected expenses. Before taking on any new debt, make sure you can afford the monthly payments. Consider the interest rate and the total cost of the loan, and compare it to other options.

4. Not Investing Your Money

Saving money is important, but it’s also important to invest it. Investing allows your money to grow over time, which can help you reach your financial goals faster. There are many different ways to invest, so it’s important to do your research and find an approach that’s right for you. If you’re not sure where to start, consider working with a financial advisor.

5. Ignoring Insurance

Insurance is a safety net that can protect you from financial ruin in case of an accident or illness. Make sure you have adequate health insurance, car insurance, and homeowner’s or renter’s insurance. If you don’t have enough insurance, you could be on the hook for large medical bills or property damage.

6. Co-signing a Loan for Someone Else

Co-signing a loan for someone else is a risky move. If the other person defaults on the loan, you’ll be responsible for paying it back. Only co-sign a loan if you’re confident that the other person can afford the payments and is a responsible borrower.

7. Making Emotional Decisions

When it comes to your finances, it’s important to make decisions based on logic, not emotion. Don’t let fear or greed cloud your judgment. Take your time, do your research, and consult with a trusted financial advisor before making any big financial decisions.

8. Falling for Scams

Scammers are always looking for ways to trick people out of their money. Be wary of any unsolicited offers, especially if they seem too good to be true. If you’re not sure whether something is a scam, do some research or consult with a financial advisor.

9. Not Planning for Unexpected Expenses

Life is full of unexpected expenses, such as car repairs, medical bills, or job loss. Not having an emergency fund can put you in a financial bind. Aim to save at least three to six months’ worth of living expenses in a savings account. This will give you a cushion to fall back

No responses yet