Introduction

Our financial choices can make or break us. But with so much information out there, it’s easy to make mistakes that can cost us dearly. From splurging on impulse buys to neglecting our retirement savings, financial missteps can have a lasting impact on our financial well-being. Don’t let these common pitfalls derail your financial goals. Read on to uncover the biggest financial mistakes people make and how to avoid them.

1. The allure of instant gratification

Have you ever found yourself swiping your credit card for something you don’t really need, just because it’s on sale? Or splurging on a fancy dinner, even though you know you can’t afford it? Welcome to the world of instant gratification – the enemy of long-term financial health. When we prioritize immediate pleasure over future financial security, we’re setting ourselves up for a cycle of debt and regret. Resist the temptation of quick fixes and focus on building a solid financial foundation instead. Remember, the gratification of a new purchase fades, but the consequences of debt can linger for years.

To avoid the trap of instant gratification, start by creating a budget and sticking to it. Track your spending and identify areas where you can cut back. Say no to unnecessary purchases and focus on saving for the future. You’ll be amazed at how quickly your financial situation can improve when you start making conscious choices about your spending.

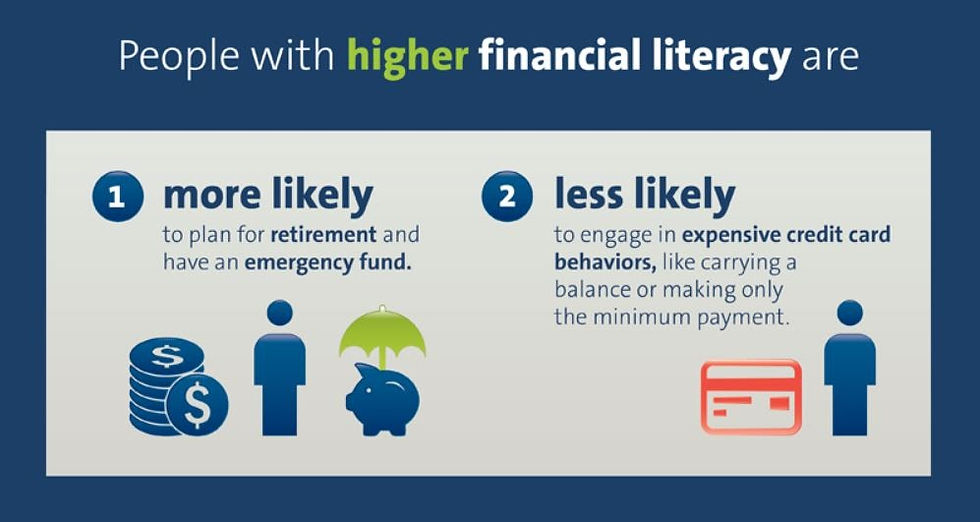

Saving for the future may seem like a distant goal, but it’s crucial to start early. The power of compound interest works in your favor over time, so even small contributions can make a big difference down the road. Set up a savings account and make regular deposits, no matter how small. It’s a simple but effective way to secure your financial future.

Retirement planning is often put on the back burner, but it’s one of the most important financial decisions you can make. The sooner you start saving, the more time your money has to grow. Don’t wait until it’s too late – start planning for your retirement today. There are various retirement savings options available, so do your research and choose the one that works best for you.

Insurance is not the most exciting topic, but it’s a crucial part of financial planning. Protect yourself from unexpected events with adequate insurance coverage. Health insurance, life insurance, and disability insurance are essential to ensure that you and your loved ones are financially protected in case of an emergency.

Investing can be a daunting task, but it’s one of the most effective ways to grow your wealth over time. Don’t let fear or lack of knowledge hold you back. Educate yourself about different investment options and seek professional advice if needed. By diversifying your investments, you can spread your risk and increase your chances of long-term success.

Common Financial Mistakes

Financial mistakes are as common as the dirt, but that doesn’t make them any less painful. In fact, a recent study found that overspending, not saving enough, and investing unwisely are the three most common financial mistakes people make. And these mistakes can have a devastating impact on our financial future.

If you’re making any of these mistakes, don’t despair. You’re not alone. And there are steps you can take to get back on track. First, let’s take a closer look at each of these mistakes and see what we can do to avoid them.

Not saving enough

If you’re not saving enough money, you’re not alone. A recent study found that over half of Americans have less than $1,000 in savings. And that’s a problem.

Without enough savings, you’re vulnerable to financial emergencies. A car repair, a medical bill, or even a job loss could send you into debt.

The good news is that it’s never too late to start saving. Even small amounts can add up over time. And there are many ways to save money, such as cutting back on unnecessary expenses, cooking at home, or shopping around for better deals.

If you’re not sure how much you should be saving, a good rule of thumb is to save at least 10% of your income. And if you can save more, all the better.

Saving money is one of the most important things you can do to secure your financial future. So don’t wait any longer. Start saving today.

Financial Mistakes People Make

Financial blunders can be a real pain in the neck, leading to a whole slew of unwelcome consequences like piling up debt, going belly up, and getting all stressed out about money. These mistakes can range from the seemingly trivial to the downright disastrous, and they can have a significant impact on our financial well-being. So, let’s dive into some of the most common financial mistakes people make and explore their potential repercussions.

Consequences of Financial Mistakes

As mentioned earlier, financial mistakes can lead to a variety of negative outcomes. These consequences can manifest in both the short and long term, and they can have a profound impact on our lives. Let’s take a closer look at some of the most common consequences of financial mistakes:

Debt

Falling into debt is one of the most common consequences of financial mistakes. When we spend more money than we have, we accumulate debt. This can quickly snowball, making it difficult to repay what we owe. High levels of debt can damage our credit scores, making it harder to qualify for loans and other forms of credit in the future. Moreover, it can lead to increased interest payments, which can further strain our finances.

Bankruptcy

In extreme cases, financial mistakes can lead to bankruptcy. Bankruptcy is a legal process that allows individuals to discharge their debts. While it can provide a way out of overwhelming debt, it also has serious consequences. Bankruptcy can stay on our credit reports for up to 10 years, making it difficult to obtain credit in the future. It can also affect our ability to get a job, rent an apartment, or even qualify for certain government benefits.

Financial Stress

Financial mistakes can also take a toll on our mental and emotional well-being. Worrying about money can lead to stress, anxiety, and even depression. Financial stress can disrupt our sleep, impair our concentration, and damage our relationships. It can also lead to unhealthy coping mechanisms, such as overeating or substance abuse.

**Don’t Make These Financial Mistakes That Can Cost You Dearly**

Oops! You slipped up. We all make financial mistakes from time to time. But some mistakes can really cost us dearly. Here are a few of the most common financial mistakes people make and how to avoid them:

Ignoring Your Budget

Creating a budget is one of the most important things you can do to manage your finances. A budget will help you track your income and expenses, so you can see where your money is going. Once you know where your money is going, you can start to make changes to save more and spend less.

Not Saving for Retirement

Retirement may seem like a long way off, but it’s never too early to start saving. The sooner you start saving, the more time your money has to grow. There are a number of different retirement savings accounts available, so you can choose one that fits your needs. Also, avoid tapping into your retirement savings early as this can have serious long-term consequences.

Investing Without a Plan

Investing is a great way to grow your wealth, but it’s important to do it wisely. Before you invest, you’ll need to develop an investment plan. Your plan should include your investment goals, risk tolerance, and time horizon. Once you have a plan, you can start investing with confidence.

Carrying Too Much Debt

Debt can be a major financial burden. If you’re carrying too much debt, it can be difficult to make ends meet. Try to avoid taking on more debt than you can afford. If you do have debt, make sure you have a plan to pay it off as quickly as possible.

Paying Only the Minimum on Your Credit Cards

When you only pay the minimum on your credit cards, you’ll end up paying more interest over time. If you want to save money on interest, try to pay off your credit cards in full each month. If you can’t pay off your credit cards in full, try to make more than the minimum payment each month.

Financial Mistakes People Unwittingly Make

You can improve your financial well-being by avoiding financial mistakes, such as impulse buying, carrying debt and not saving money. It sounds simple enough, right? However, many people unknowingly make these financial blunders, potentially jeopardizing their financial well-being. Here are some tips to help you avoid these common financial pitfalls and reach your financial destinations.

Living Beyond Your Means

One of the most common financial mistakes is living beyond your means. There’s nothing inherently wrong with enjoying the finer things in life. But when you consistently spend more than you earn, you’re setting yourself up for financial hardship. To avoid this trap, create a budget that tracks your income and expenses. This will help you ensure that you’re not overspending and that you’re saving for the future.

Not Saving Money

Saving money is essential for financial security. It’s the key to having a cushion for unexpected expenses, reaching financial goals, and retiring comfortably. Yet, many people don’t save enough money or, unfortunately, don’t save any at all. If you’re not saving money, now’s the time to start. Even small amounts can add up to make a big difference over time.

Impulse Buying

We all know that feeling – you see something you like, and you just have to have it. But before you make that purchase, ask yourself if you really need it. Impulse buying can quickly lead to debt and financial problems. If you’re struggling with impulse buying, try to give yourself a cooling-off period before you buy anything. This will help you make more informed decisions about your spending.

Carrying Debt

Debt is a major financial burden. High-interest rates can make it difficult to get ahead financially. If you’re carrying debt, try to pay it off as quickly as possible. There are tons of resources available to help you get out of debt, so don’t be afraid to seek help if you need it.

Not Investing

Investing is one of the best ways to grow your wealth. Over time, the stock market has consistently outperformed other investments, such as savings accounts and bonds. If you’re not investing, you’re missing out on opportunities to grow your money. There are many different ways to invest, so do some research and find a strategy that works for you.

Conclusion

By avoiding these common financial mistakes, you can improve your financial well-being and achieve your financial goals. Improving your financial well-being is a process, not an event. There will be setbacks along the way, but don’t give up. Just keep working at it, and you will eventually reach your goals.

No responses yet