**

Retirement Plan vs 401k

**

Retirement planning is a crucial aspect of financial well-being, ensuring a secure future beyond working years. When considering retirement options, individuals encounter two common terms: retirement plan and 401k. Understanding the distinctions between these concepts is essential for making informed decisions. While both aim to facilitate saving and investing for retirement, they differ in their structures and benefits, creating unique advantages and considerations for various individuals. Let’s delve into the nuances of each concept, exploring their similarities and differences.

**

What is a Retirement Plan?

**

A retirement plan is a comprehensive strategy that involves saving and investing money specifically for post-retirement expenses. It offers a structured approach to accumulate funds that can supplement or replace regular income when an individual stops working. Retirement plans come in diverse forms, catering to different needs and financial situations. Some common types include 401k plans, traditional IRAs, Roth IRAs, and annuities. Each plan carries its own set of rules and tax implications, so it’s imperative to research and select the most suitable option for individual circumstances.

Retirement plans typically involve contributions from both the employee and, in some cases, the employer. Contributions may be pre-tax or post-tax, affecting the immediate and future tax implications. Earnings within the plan grow tax-deferred or tax-free, depending on the plan type, allowing for potential long-term growth. Upon retirement, individuals can access their accumulated funds through withdrawals, which may be subject to taxes based on the plan’s structure.

The primary objective of a retirement plan is to provide financial security during retirement years. By setting aside funds regularly and taking advantage of tax benefits, individuals can build a solid financial foundation for their golden years. Retirement plans offer flexibility and control, allowing individuals to tailor their savings strategies to their specific goals and risk tolerance.

In summary, a retirement plan is a long-term financial strategy designed to accumulate funds specifically for retirement expenses. It offers various options to suit individual needs, providing tax benefits and growth potential for securing a financially comfortable retirement.

Retirement Plan vs. 401k: Which is Right for You?

Ah, retirement. A time to kick back, relax, and finally enjoy the fruits of your labor. But how do you get there? One way is to start saving early and often. That’s where retirement plans come in. But which one is right for you? Let’s take a look at two popular options: retirement plans and 401ks.

Types of Retirement Plans

Retirement plans come in all shapes and sizes. There are IRAs, 401ks, annuities, and pensions. Each type of plan has its own unique set of benefits and drawbacks. So, it’s important to do your research and choose the one that’s right for you.

401k Plans: What You Need to Know

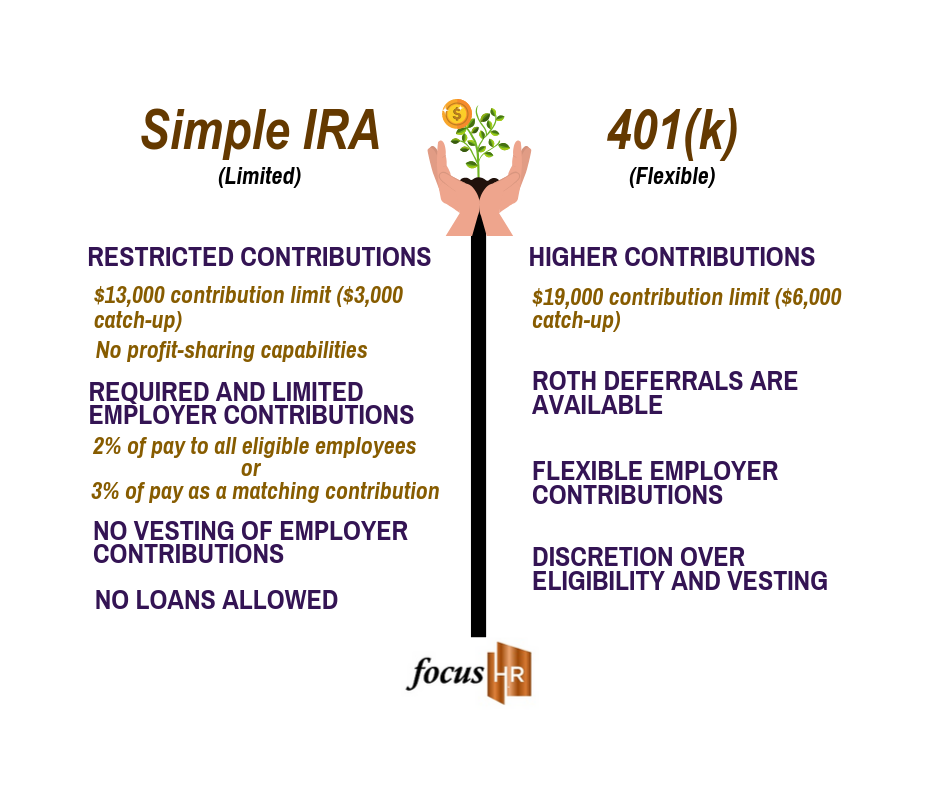

401k plans are one of the most popular retirement savings plans in the United States. They’re offered by many employers, and they allow you to save money pre-tax. This means that you can reduce your taxable income and save more for retirement. 401k plans also offer a variety of investment options, so you can choose the ones that are right for your risk tolerance and investment goals. But there are some things to keep in mind with 401k plans. First, they have contribution limits. In 2023, the limit is $22,500 ($30,000 if you’re age 50 or older). Second, there are penalties for early withdrawal. If you withdraw money from your 401k before you’re 59 1/2, you’ll have to pay a 10% penalty, plus income tax on the withdrawal.

Retirement Plan vs 401K: Which Is the Right Choice for You?

As you approach retirement, saving and investing is crucial for ensuring a secure financial future. Retirement plans, such as 401Ks, offer tax benefits, investment options, and potential employer contributions to help you build your nest egg. However, it’s important to understand the differences between retirement plans and 401Ks to make an informed decision about which is right for your unique needs.

Benefits of a 401K

401Ks are employer-sponsored retirement plans that offer several attractive benefits. Firstly, they provide tax advantages. Contributions to a traditional 401k are tax-deductible, reducing your current taxable income. Additionally, earnings in a 401k grow tax-deferred, meaning you won’t pay taxes on them until you withdraw them in retirement.

Secondly, 401Ks offer the potential for employer matching contributions. Many employers match a portion of their employees’ contributions, up to a certain limit. This is essentially free money that can significantly boost your retirement savings.

Thirdly, 401Ks offer a wide range of investment options. You can choose from stocks, bonds, mutual funds, and other investments to diversify your portfolio and align it with your risk tolerance and financial goals. With a 401K, you have the flexibility to tailor your investments to your individual needs and preferences.

Retirement Plan vs. 401k

When it comes to planning for retirement, there are many different options available. Two of the most popular options are a retirement plan and a 401k. But what’s the difference between the two? And which one is right for you?

401k

A 401k is a retirement savings plan offered by many employers. It allows employees to save money for retirement on a pre-tax basis, meaning that the money is deducted from your paycheck before taxes are taken out. This can save you a significant amount of money on taxes over time.

401ks are subject to annual contribution limits, and the amount that you can contribute each year is based on your age and the type of plan you have. There are two types of 401k plans: traditional and Roth. Traditional 401ks allow you to take a tax deduction for your contributions, but you have to pay taxes on the money when you withdraw it in retirement. Roth 401ks, on the other hand, allow you to contribute after-tax dollars, but your withdrawals in retirement are tax-free.

Eligibility for a 401k

Eligibility for a 401k depends on several factors, including your employment status, age, and income. You must be an employee of a company that offers a 401k plan in order to participate. You must also be at least 21 years old and have worked for the company for at least one year. There are no income limits for participation in a 401k plan.

Contribution Limits

The amount you can contribute to a 401k each year is limited by the IRS. For 2022, the contribution limit is $20,500. If you are age 50 or older, you can make an additional catch-up contribution of $6,500.

Investment Options

401k plans offer a variety of investment options, including stocks, bonds, and mutual funds. The investment options that you choose will depend on your risk tolerance and time horizon. If you are younger and have a longer time horizon, you may want to invest in more aggressive options, such as stocks. If you are closer to retirement, you may want to invest in more conservative options, such as bonds.

Fees

401k plans can have fees associated with them, such as administrative fees and investment fees. These fees can vary from plan to plan, so it is important to compare the fees of different plans before you choose one.

Retirement Plan vs. 401k: What’s the Difference?

Retirement plans, such as 401ks, are essential tools for securing a comfortable financial future. While these terms are often used interchangeably, there are some key distinctions between them.

Contribution Limits

401ks impose annual contribution limits, which are subject to fluctuations based on factors like age and income. For 2023, the contribution limit for individuals under 50 is $22,500, and for those 50 and older, it’s $30,000. These limits include both employee and employer contributions.

Employer Matching

One major advantage of 401ks over other retirement plans is employer matching. Employers may contribute a portion of your salary to your 401k, up to a certain limit. This “free” money can significantly boost your retirement savings.

Investment Options

401ks typically offer a range of investment options, including stocks, bonds, and mutual funds. This allows you to tailor your investments to your risk tolerance and financial goals.

Withdrawal Rules

Unlike traditional IRAs, 401ks generally have stricter withdrawal rules. Early withdrawals (before age 59½) may incur a 10% penalty. However, there are some exceptions, such as withdrawals for qualified medical expenses or disability.

Portability

401ks are portable, meaning you can take them with you when you change jobs. This provides flexibility and ensures that your retirement savings remain intact.

Which One Is Right for You?

The best retirement plan for you depends on your individual circumstances and financial goals. If you have access to a 401k with employer matching, it’s generally a wise choice due to the potential for additional savings. However, if you need more flexibility or have a high risk tolerance, an IRA may be a better option.

**Retirement Plan vs. 401k: A Comprehensive Guide**

Retirement planning is an essential part of securing your financial future. Two common options are retirement plans and 401ks. While both can help you save for retirement, they have key differences that can impact your decision.

**What’s the Difference?**

Retirement plans are employer-sponsored plans that allow employees to contribute pre-tax dollars. These contributions grow tax-deferred, meaning you won’t pay taxes on them until you withdraw them in retirement. 401ks are a type of retirement plan specifically designed for private-sector employees. They offer similar tax advantages and investment options, but may have different contribution limits and investment choices than other retirement plans.

Investment Options

401ks offer a wide range of investment options, including:

- Stocks: Individual shares of companies that have the potential for growth but also carry risk.

- Bonds: Loans made to companies or governments that offer lower returns but generally less risk than stocks.

- Mutual funds: Baskets of stocks or bonds that are managed by professional fund managers.

- Index funds: Funds that track the performance of a particular market index, such as the S&P 500.

- Target-date funds: Funds that automatically adjust the asset allocation based on your age and retirement date.

- Stable value funds: Funds that invest in low-risk assets, such as cash and short-term bonds, and are designed to protect principal.

Each investment option has its own risks and rewards. It’s important to carefully consider your risk tolerance and retirement goals when choosing investments.

Retirement Plan vs. 401(k): Which Is Right for You?

So, you’ve finally reached the point in your career where you’re starting to think about retirement. Congratulations! Now comes the fun part: figuring out how to save for it. There are a lot of different retirement plans out there, like 401(k)s and 403(b)s, and it can be tough to know which one is right for you. That’s why we’re here to help!

Choosing the Right Plan

The best retirement plan for you depends on your individual circumstances and financial goals. Here are a few things to consider:

- Your age: The sooner you start saving for retirement, the better. But don’t worry if you’re starting late. There are still plenty of ways to catch up.

- Your income: If you have a high income, you may want to consider a traditional 401(k) or 403(b). These plans allow you to contribute more money than Roth accounts.

- Your tax bracket: If you’re in a high tax bracket, you may want to consider a Roth account. These accounts allow your money to grow tax-free.

- Your risk tolerance: If you’re not comfortable with the ups and downs of the stock market, you may want to consider a more conservative retirement plan, such as a money market account or CD.

Traditional 401(k)s

Traditional 401(k)s are employer-sponsored retirement plans that allow you to contribute pre-tax dollars. This means you don’t pay taxes on the money you contribute until you withdraw it in retirement. 401(k)s are a great way to save for retirement because they offer a number of tax benefits.

Roth 401(k)s

Roth 401(k) are similar to traditional 401(k)s, but there are a few key differences. Roth 401(k) plans offer tax-free growth, but contributions are made on an after-tax basis. This means you pay taxes on the money you contribute, but your earnings grow tax-free and you don’t pay any taxes when you withdraw the money in retirement. Roth 401(k)s are a good option for people who expect to be in a higher tax bracket in retirement.

403(b) Plans

403(b) plans are similar to 401(k) plans in every shape and form, including the way they work and the type of investments they offer. The main difference is that 403(b) plans are available to employees of public schools and certain other tax-exempt organizations.

IRAs

IRAs(Traditional and Roth) are individual retirement accounts that allow you to save for retirement on a tax-advantaged basis. Traditional IRAs offer tax-deferred growth, while Roth IRAs offer tax-free growth. IRAs are a good option for people who don’t have access to an employer-sponsored retirement plan.

Choosing the Right Plan for You

The best retirement plan for you depends on your individual circumstances and financial goals. Consider your age, income, tax bracket, and risk tolerance when making a decision. If you’re not sure which plan is right for you, talk to a financial advisor.

Retirement Plans vs. 401ks: A Comprehensive Guide

When it comes to planning for your golden years, you have a few different options to choose from. Two of the most popular options are retirement plans and 401ks. But what’s the difference between the two? And which one is right for you?

In this article, we’ll take a detailed look at retirement plans and 401ks, so you can make an informed decision about which one is right for you.

What is a Retirement Plan?

A retirement plan is a tax-advantaged account that allows you to save for your retirement. There are many different types of retirement plans, including 401ks, IRAs, and pensions.

What is a 401k?

A 401k is a type of retirement plan that is offered by employers. With a 401k, you can contribute a portion of your paycheck to the plan on a pre-tax basis. This means that the money you contribute to your 401k is not taxed until you withdraw it in retirement.

Key Differences Between Retirement Plans and 401ks

There are a few key differences between retirement plans and 401ks. Here’s a breakdown:

- Eligibility: Retirement plans are available to everyone, regardless of their employment status. 401ks are only available to employees of companies that offer the plan.

- Contribution limits: The contribution limits for retirement plans are generally higher than the contribution limits for 401ks.

- Investment options: Retirement plans offer a wider range of investment options than 401ks.

- Tax advantages: Retirement plans and 401ks both offer tax advantages. However, the tax advantages of 401ks are generally more generous.

- Early withdrawal penalties: Retirement plans and 401ks both have early withdrawal penalties. However, the early withdrawal penalties for 401ks are generally more severe.

Which One is Right for You?

The best way to decide which type of retirement plan is right for you is to consider your individual circumstances. If you’re not sure which type of plan is right for you, talk to a financial advisor.

Contribution Limits

The contribution limits for retirement plans and 401ks vary depending on the type of plan and your age. For 2023, the contribution limits are as follows:

Retirement plans:

- Traditional IRA: $6,500 ($7,500 if you’re age 50 or older)

- Roth IRA: $6,500 ($7,500 if you’re age 50 or older)

401ks:

- Employee elective deferrals: $22,500 ($30,000 if you’re age 50 or older)

- Employer matching contributions: $66,000 ($73,500 if you’re age 50 or older)

Investment Options

Retirement plans and 401ks offer a variety of investment options. The investment options that are available to you will depend on the plan you choose. Some common investment options include:

- Stocks

- Bonds

- Mutual funds

- Exchange-traded funds (ETFs)

Tax Advantages

Retirement plans and 401ks both offer tax advantages. With a retirement plan, you can contribute money on a pre-tax basis. This means that the money you contribute to your plan is not taxed until you withdraw it in retirement. With a 401k, you can also contribute money on a pre-tax basis. In addition, your employer may make matching contributions to your 401k. These matching contributions are not taxed until you withdraw them in retirement.

Early Withdrawal Penalties

Retirement plans and 401ks both have early withdrawal penalties. If you withdraw money from your plan before you reach age 59½, you may have to pay a 10% penalty. However, there are some exceptions to this rule. For example, you can withdraw money from your plan without paying a penalty if you use the money to pay for qualified expenses, such as medical expenses or higher education expenses.

Conclusion

Retirement plans and 401ks are valuable tools for building a financially secure retirement. They offer a variety of tax advantages and investment options. The best way to decide which type of plan is right for you is to consider your individual circumstances. If you’re not sure which type of plan is right for you, talk to a financial advisor.

No responses yet