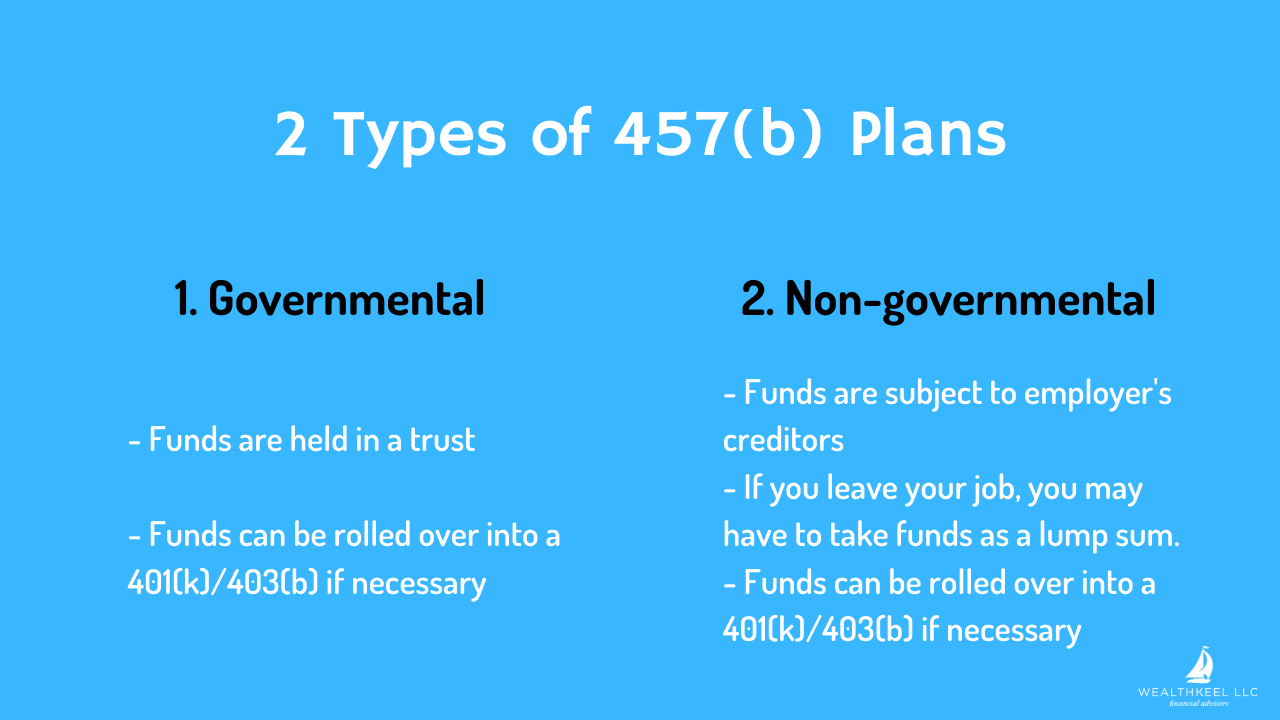

457 Retirement Plan

If you are employed by state or local governments and specific non-profit organizations, you may have the privilege of accessing a 457 retirement plan or deferred compensation plan. This tax-advantaged retirement savings plan is exclusively available to you, and understanding its intricacies can empower you to make informed decisions about your financial future.

Who Qualifies for a 457 Plan?

To be eligible for a 457 plan, you must meet the following criteria:

-You must be an employee of any state, county, or municipality within the United States.

– You must be working for a tax-exempt, non-profit organization.

How Does a 457 Plan Work?

Contributions made to a 457 retirement plan are deducted from your salary on a pre-tax basis. This means that your taxable income is reduced by the amount you contribute, resulting in lower current taxes. The earnings on your investments within the plan also grow tax-deferred until you withdraw them in retirement.

Unlike 401(k) plans, which have annual contribution limits, 457 plans offer no such restrictions. However, there are annual limits on the amount that can be contributed on a pre-tax basis. For 2023, the elective contribution limit is $22,500, and the catch-up contribution limit for those age 50 or older is $7,500.

Withdrawals from a 457 plan can be made once you reach age 59½, retire, become disabled, or experience financial hardship. However, withdrawals before age 59½ may be subject to a 10% early withdrawal penalty, and income taxes are due on the amount withdrawn.

Benefits of a 457 Plan

457 plans offer several advantages that make them attractive retirement savings options:

-Tax-deferred savings: Contributions are made before taxes, reducing your current taxable income and allowing your investments to grow tax-deferred.

– High contribution limits: 457 plans have generous contribution limits compared to other retirement plans, which enables you to save more for retirement.

-Employer contributions: Some employers offer matching contributions to 457 plans, providing you with an additional boost to your retirement savings.

-No required minimum distributions: Unlike traditional IRAs and 401(k) plans, 457 plans do not have required minimum distributions, giving you more flexibility in managing your retirement income.

457 Retirement Plan: A Comprehensive Overview for Informed Decision-Making

Amidst the labyrinthine array of retirement savings options, 457 retirement plans stand out as a powerful tool for tax-advantaged savings. These plans, designed exclusively for employees of government entities and certain tax-exempt organizations, offer unparalleled benefits. But before embarking on this financial journey, it’s imperative to unravel the intricacies of 457 plans. This comprehensive guide will illuminate the eligibility requirements, investment options, and tax implications, empowering you to make informed decisions about your retirement future.

Eligibility: An Inclusive Approach

The doors of 457 retirement plans are open to a wide swath of individuals. Employees of federal, state, and local government agencies, as well as those working for eligible non-profit organizations, are prime candidates for these plans. Moreover, there are no age or income restrictions, making 457 plans an accessible savings vehicle for individuals at all stages of their careers.

Investment Options: Customizing Your Savings Strategy

457 retirement plans offer a diverse range of investment options, granting participants the flexibility to craft a portfolio that aligns with their risk tolerance and financial objectives. From traditional options such as stocks and bonds to more unconventional investments like real estate and alternative assets, participants have ample choices to tailor their savings strategy. The specific investment options available may vary depending on the plan sponsor, but the overall breadth of choices ensures that every participant can find suitable investment vehicles.

Tax Benefits: A Path to Tax-Favored Savings

One of the most compelling reasons to consider a 457 retirement plan lies in its tax advantages. Contributions to 457 plans are made pre-tax, meaning they are deducted from your paycheck before taxes are calculated. This reduction in taxable income can result in significant tax savings, particularly for individuals in higher tax brackets. Additionally, earnings within a 457 plan grow tax-deferred, meaning you won’t pay taxes on the investment returns until you withdraw funds in retirement. This tax deferral allows your savings to compound more rapidly, potentially leading to a larger retirement nest egg.

Contribution Limits: Understanding the Parameters

While 457 retirement plans offer substantial benefits, it’s important to be aware of the contribution limits. For 2023, the annual contribution limit for 457 plans is $22,500. Participants age 50 or older are eligible for catch-up contributions of an additional $7,500, bringing their total annual contribution limit to $30,000. These limits help ensure that 457 plans are used for retirement savings and not as a tax avoidance scheme.

Withdrawal Rules: Striking a Balance

Accessing funds from a 457 retirement plan is subject to certain rules. Generally, withdrawals are permitted after the participant reaches age 59½. Withdrawals prior to that age may be subject to a 10% penalty tax, although there are exceptions for certain circumstances such as disability or hardship. It’s crucial to understand these withdrawal rules and plan accordingly to avoid potential tax consequences.

Conclusion: A Wise Investment for a Secure Retirement

457 retirement plans are a strategic financial tool for individuals seeking tax-advantaged retirement savings. With eligibility open to a broad range of employees, diverse investment options, and significant tax benefits, 457 plans offer a compelling path to financial security in retirement. By carefully considering the eligibility requirements, investment options, and tax implications, you can harness the power of 457 plans to build a substantial retirement fund and enjoy a more prosperous future.

What is a 457 Retirement Plan?

A 457 retirement plan is a tax-advantaged savings plan designed for employees of state and local governments and certain other tax-exempt organizations. If you’re eligible for a 457 plan, it’s a smart way to save for retirement, especially if you don’t have access to other retirement savings plans, like a 401(k) plan. Contributions to a 457 plan are made on a pre-tax basis, which reduces your current taxable income. This means you’ll pay less in taxes now and more in retirement when you’re in a lower tax bracket.

Contributions

As an eligible employee, you can contribute up to $22,500 to your 457 plan in 2023. This limit is set by the IRS and is adjusted annually for inflation. If you’re age 50 or older, you can contribute an additional $7,500 as a catch-up contribution. This means you can contribute a total of $30,000 to your 457 plan in 2023 if you’re eligible.

Contributions to a 457 plan are made on a pre-tax basis, which means they’re deducted from your paycheck before taxes are taken out. This reduces your current taxable income, which can save you a significant amount of money in taxes. For example, if you contribute $5,000 to your 457 plan and you’re in a 25% tax bracket, you’ll save $1,250 in taxes.

In addition to the regular contribution limit, you may also be eligible to make catch-up contributions if you’re age 50 or older. Catch-up contributions are designed to help you save more for retirement if you’ve fallen behind on your retirement savings. In 2023, the catch-up contribution limit for 457 plans is $7,500. This means you can contribute a total of $30,000 to your 457 plan if you’re age 50 or older.

Catch-up contributions are also made on a pre-tax basis, which means they’re deducted from your paycheck before taxes are taken out. This can save you a significant amount of money in taxes, especially if you’re in a high tax bracket.

If you’re eligible for a 457 plan, it’s a smart way to save for retirement. Contributions to a 457 plan are made on a pre-tax basis, which reduces your current taxable income. This can save you a significant amount of money in taxes, especially if you’re in a high tax bracket.

**457 Retirement Plans: A Comprehensive Guide**

457 plans offer a tax-advantaged way to save for retirement, but they can be a bit complex. This guide will help you understand how 457 plans work, the investment options available, and the benefits they offer.

**What is a 457 Retirement Plan?**

A 457 plan is a tax-advantaged retirement plan that is offered by state and local governments and certain other tax-exempt organizations. Contributions to a 457 plan are made on a pre-tax basis, meaning they are deducted from your paycheck before taxes are taken out. This can reduce your current taxable income and save you money on taxes.

**Investment Options**

457 plans typically offer a variety of investment options, allowing participants to choose investments that align with their risk tolerance and financial goals. Some common investment options include:

* **Mutual funds:** Mutual funds are professionally managed investment funds that pool money from multiple investors and invest in a variety of assets, such as stocks, bonds, and real estate.

* **Exchange-traded funds (ETFs):** ETFs are similar to mutual funds, but they are traded on exchanges like stocks.

* **Target-date funds:** Target-date funds are mutual funds that automatically adjust their investment mix based on the participant’s expected retirement date.

* **Fixed annuities:** Fixed annuities provide a guaranteed rate of return over a specified period of time.

* **Variable annuities:** Variable annuities offer the potential for higher returns, but they are also subject to more risk.

**Benefits of 457 Retirement Plans**

There are a number of benefits to contributing to a 457 retirement plan, including:

* **Tax savings:** Contributions to a 457 plan are made on a pre-tax basis, which can reduce your current taxable income and save you money on taxes.

* **Tax-free growth:** Earnings on your 457 plan grow tax-free until you withdraw them in retirement.

* **Employer contributions:** Some employers may make matching contributions to their employees’ 457 plans.

* **Flexibility:** 457 plans offer a variety of investment options, so you can choose investments that align with your risk tolerance and financial goals.

* **Catch-up contributions:** Participants who are age 50 or older can make additional catch-up contributions to their 457 plans.

**457 Retirement Plans: A Comprehensive Guide to Saving for Retirement**

Are you seeking a tax-advantaged retirement savings plan? Look no further than the 457 retirement plan. Specifically designed for employees of state and local governments, as well as certain non-profit organizations, this plan offers numerous benefits that can help you secure your financial future.

**Tax Benefits**

The 457 plan stands out for its substantial tax advantages. Contributions to the plan are made on a pre-tax basis, meaning they are deducted from your paycheck before taxes are calculated. This reduces your current taxable income, saving you money on income taxes.

**Contribution Limits**

The IRS sets annual limits on how much you can contribute to your 457 plan. For 2023, the limit is $22,500. However, individuals who are age 50 or older can make catch-up contributions of up to $3,500.

**Investment Options**

457 plans typically offer a wide range of investment options, including stocks, bonds, mutual funds, and annuities. This allows you to customize your investments to match your risk tolerance and retirement goals.

**Employer Contributions**

In some cases, employers may choose to make matching contributions to their employees’ 457 plans. These contributions are not included in your taxable income and can significantly boost your retirement savings.

**Withdrawals**

Withdrawals from a 457 plan can be made after you reach age 59.5. Distributions are taxed as ordinary income, but there are exceptions for certain circumstances, such as a qualified medical emergency.

**Benefits of 457 Retirement Plans**

* **Tax savings:** Reduce your current taxable income and save on income taxes.

* **Retirement savings:** Accumulate a significant nest egg for your golden years.

* **Investment flexibility:** Choose from a wide range of investment options to meet your needs.

* **Employer matching contributions:** Potential for additional retirement savings from your employer.

* **Tax-free growth:** Your investments grow tax-deferred until withdrawals are made.

* **Estate planning:** 457 plans can be included in your estate planning strategies to pass on assets to your beneficiaries.

**Eligibility**

To be eligible for a 457 plan, you must be an employee of a state or local government, or a non-profit organization that participates in the plan. If your employer does not offer a 457 plan, you may want to consider other tax-advantaged retirement savings options, such as the 403(b) plan or the 401(k) plan.

**Conclusion**

The 457 retirement plan is an excellent savings vehicle for eligible employees. With its tax advantages, contribution limits, investment options, and potential for employer matching contributions, it can help you save significantly for your retirement. If you have the opportunity to participate in a 457 plan, don’t hesitate to take advantage of its benefits and secure your financial future.

Introduction

Planning for retirement is a critical step toward financial security in the golden years. Among the various retirement savings options available, the 457 plan stands out as a valuable tool for government and nonprofit employees. This article delves into the intricacies of the 457 retirement plan, specifically exploring the distribution options available to participants.

Distribution Options

Participants in a 457 plan can begin withdrawing funds at age 55 without incurring a 10% early withdrawal penalty. However, it’s not mandatory to start taking distributions at this age. Participants can delay distributions until age 72, but they must take at least one distribution by the end of that year.

Traditional Distributions

The most straightforward distribution method is to withdraw funds directly from the 457 plan account. These distributions are subject to ordinary income tax rates, and they can be made in a lump sum or in periodic payments.

Roth Distributions

Roth 457 plans offer tax-free distributions in retirement. However, contributions to Roth 457 plans are made after-tax, meaning they are not tax-deductible upfront. To qualify for tax-free Roth distributions, participants must avoid taking any distributions before age 59½ or wait five years after their first Roth 457 contribution, whichever comes later.

In-Service Distributions

While most distributions from 457 plans are taken during retirement, limited exceptions allow for in-service distributions in certain cases. For example, participants may be able to withdraw funds to cover medical expenses or to purchase a primary residence.

Required Minimum Distributions

Once participants reach age 72, they must begin taking required minimum distributions (RMDs) from their 457 plan account. Failure to take RMDs can result in penalties.

Other Distribution Options

In addition to the primary distribution options, participants in 457 plans may also have the option to receive loans or annuities from their account. These distribution methods have specific rules and requirements, and they should be carefully considered before being implemented.

Conclusion

The 457 retirement plan provides participants with a valuable tool for saving for retirement. Understanding the distribution options available is essential for maximizing the potential benefits of a 457 plan. By carefully considering the various distribution methods and their potential tax implications, participants can effectively plan for a secure financial future.

**457 Retirement Plan: Navigating Tax Implications and Early Withdrawals**

A 457 retirement plan is a tax-advantaged savings vehicle designed specifically for government employees and certain non-profit organizations. These plans offer valuable tax benefits and can assist in accumulating funds for retirement. However, understanding the tax implications associated with withdrawals is crucial to avoid potential penalties and maximize the plan’s benefits.

Early Withdrawal

Withdrawing funds from a 457 plan before reaching age 59½ typically incurs a 10% early withdrawal penalty tax on top of the regular income tax liability. This penalty can significantly erode the value of your retirement savings. Exceptions to this penalty include withdrawals made after separation from service (age 55 or older), withdrawals made due to disability, and certain qualified distributions for medical expenses, educational expenses, or first-time home purchases.

In addition to the 10% penalty tax, early withdrawals from a 457 plan may also be subject to federal income tax. Depending on the individual’s tax bracket, the combined tax liability on early withdrawals can be substantial. Therefore, it is generally advisable to avoid early withdrawals from a 457 plan unless absolutely necessary.

For example, if you withdraw $10,000 from your 457 plan at age 50, you could face a $1,000 penalty tax plus ordinary income tax on the withdrawal. This could result in a total tax liability of over $3,000, depending on your tax bracket.

If you’re considering an early withdrawal from your 457 plan, carefully weigh the potential tax implications and explore all other options. Consulting with a financial advisor can provide valuable guidance and help you make informed decisions about your retirement savings.

No responses yet