Alternative Retirement Plans: Breaking Free from the Traditional Mold

Don’t get stuck in a retirement rut! While traditional plans like 401(k)s and IRAs have their perks, they’re not the only game in town. Let’s explore some alternative retirement plans that can help you diversify your savings and secure your golden years.

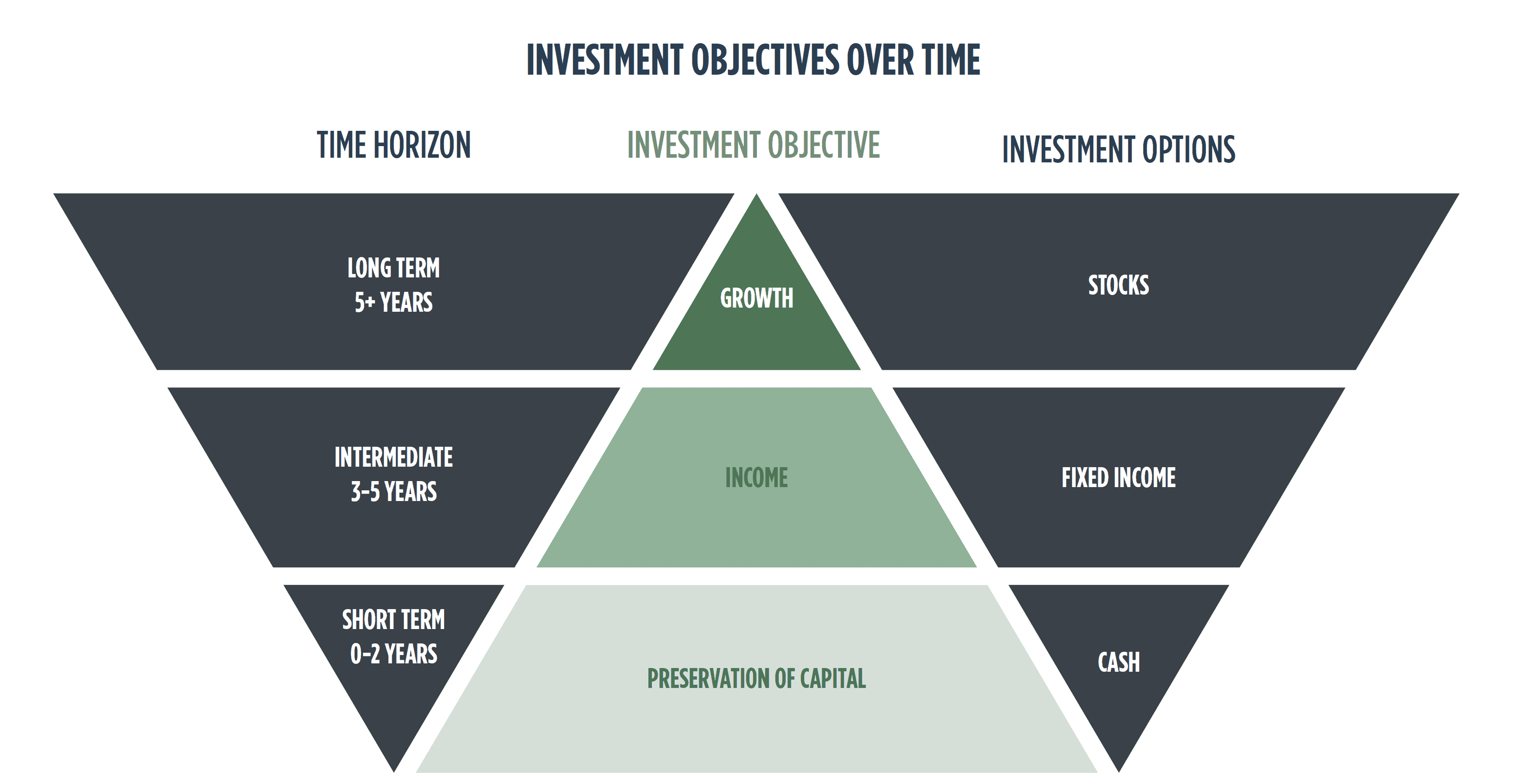

Traditional Retirement Plans

Traditional retirement plans offer tax breaks and potential for growth, but they can also come with restrictions and penalties. For instance, early withdrawals from a 401(k) before age 59½ can incur a 10% penalty tax. Plus, traditional IRAs have income limits that can affect your contributions.

Moreover, traditional plans often limit your investment options, tying you to specific funds or annuities. This can hinder your ability to customize your portfolio and maximize returns. And don’t forget about the potential impact of market volatility, which can erode your savings if you’re not prepared.

So, what’s a savvy investor to do? It’s time to consider some alternative retirement plans that offer more flexibility, control, and potential growth.

Alternative Retirement Plans

Now that you’ve worked hard and saved diligently for retirement, you may be wondering if there are any other options besides traditional retirement plans like 401(k)s and IRAs. The answer is a resounding yes! Alternative retirement plans can offer a wider range of investment choices, greater flexibility, and potential tax advantages. One popular alternative is the Roth IRA, which allows you to contribute after-tax dollars and then withdraw them tax-free in retirement. Annuities are another option, providing a guaranteed income stream for life in exchange for a lump sum investment. Real estate investments can also be a lucrative retirement strategy, offering the potential for both capital appreciation and rental income. So, if you’re looking to diversify your retirement portfolio and maximize your nest egg, here are some alternative retirement plans worth considering!

Annuities: A Guaranteed Income Stream for Life

An annuity is a contract with an insurance company that provides you with a regular income stream for life or a specified period. In exchange for a lump sum investment, the insurance company agrees to make payments to you starting at a future date, regardless of how long you live. Annuities can be a great way to ensure that you have a steady income in retirement, even if your other investments perform poorly. They are also a good way to protect yourself against inflation, as the payments can be adjusted to keep pace with the cost of living.

There are two main types of annuities: immediate annuities and deferred annuities. Immediate annuities begin making payments to you right away, while deferred annuities allow you to accumulate money tax-deferred until you start taking withdrawals. Deferred annuities can be a good option if you are still working and want to maximize your tax savings.

Annuities can be a valuable part of a diversified retirement portfolio. However, it is important to understand the different types of annuities and how they work before you invest. You should also compare the costs and benefits of annuities with other retirement savings options.

**Alternative Retirement Plans: Breaking the Mold**

Retirement planning is no longer a one-size-fits-all endeavor. As traditional retirement plans like 401(k)s and pensions continue to evolve, individuals are exploring alternative retirement plans that cater to their unique financial goals. If you’re looking to break free from the conventional retirement mold, here are a few options worth considering:

Roth Accounts

Roth accounts, such as Roth IRAs and Roth 401(k)s, have gained immense popularity due to their tax-free withdrawals in retirement. Unlike traditional retirement accounts that tax withdrawals at your current income rate, Roth accounts allow you to withdraw your contributions tax-free, irrespective of the size of your nest egg. This makes Roth accounts ideal for those who anticipate being in a higher tax bracket during their retirement years.

Roth accounts also offer greater flexibility compared to traditional retirement plans. You can contribute to Roth accounts after reaching age 59½, and there are no required minimum distributions (RMDs) during your lifetime. However, contributions to Roth accounts are subject to income limits, and you may face a tax penalty if you withdraw earnings before reaching age 59½.

Traditional IRAs

Traditional IRAs are another retirement savings option that allows you to save for retirement on a tax-advantaged basis. With traditional IRAs, you receive a tax deduction on your contributions upfront, but your withdrawals in retirement are taxed at your current income rate. Traditional IRAs are a good option for those who expect to be in a lower tax bracket in retirement or who will need the tax deduction to maximize their retirement savings.

Traditional IRAs offer similar flexibility to Roth accounts, allowing you to contribute after reaching age 59½ and without required minimum distributions during your lifetime. However, contributions to traditional IRAs are not subject to income limits, and there are no tax penalties for early withdrawals, although you will have to pay taxes on the withdrawn amount.

Annuities

Annuities are insurance contracts that provide you with a guaranteed stream of income in retirement. When you purchase an annuity, you make a lump sum payment or a series of smaller payments. In return, the insurance company promises to pay you a set amount of money each month for as long as you live. Annuities can be a good option for those who want guaranteed income in retirement but are concerned about outliving their savings.

Annuities come with different features and options, so it’s important to carefully consider your needs before purchasing one. Some annuities offer a death benefit, which means that your beneficiaries will receive money if you die before the annuity period ends. Other annuities offer inflation protection, which means that your monthly payments will increase over time to keep pace with inflation.

Alternative Retirement Plans: Diversify Your Nest Egg

When it comes to retirement planning, don’t get stuck in a rut. Explore alternative retirement plans that can complement your traditional options and diversify your financial future.

Annuities

Annuities are like financial insurance policies that guarantee a regular income stream in retirement. They’re like a financial river that keeps flowing, no matter what storms life throws your way. But like any insurance, annuities come with a price. They can be pricey and inflexible, so it’s crucial to weigh the pros and cons before diving in.

Cash Value Life Insurance

Cash value life insurance is a two-for-one deal: it provides both life insurance coverage and a tax-advantaged savings account. It’s like having a retirement stash tucked away within your insurance policy. The cash value grows tax-deferred, giving you a potential source of funds in your golden years.

Real Estate

Real estate can be a solid investment for retirement. It offers potential income through rent and appreciation, and it can serve as a long-term hedge against inflation. However, it’s not without its challenges. Managing properties can be time-consuming, and market downturns can hurt your returns.

Dividend-Paying Stocks

Dividend-paying stocks are like miniature cash machines that pay you regular dividends. They can provide a steady income stream and grow in value over time. But remember, the stock market is a roller coaster, so don’t put all your eggs in one basket. Diversify your stock portfolio and invest for the long haul.

Don’t Put All Your Eggs in One Basket

The key to a successful retirement is diversification. Don’t rely solely on one plan. Blend different strategies to create a balanced portfolio that meets your unique needs and goals. Consider alternative retirement plans to enhance your financial security and enjoy a worry-free retirement.

**Alternative Retirement Plans: Breaking Away From the Norm**

Retirement planning often conjures images of traditional 401(k)s and IRAs, but savvier investors are exploring alternative avenues to secure their financial future. From real estate investments to dividend-paying stocks, the options are varied, each offering unique advantages and drawbacks. Let’s delve into these alternatives, starting with the one that’s as solid as the ground beneath our feet: real estate.

Real Estate Investments

Real estate has long been a popular retirement investment for its potential to generate rental income and appreciate in value. However, it’s not without its challenges. Buying rental properties requires a substantial upfront investment and necessitates ongoing maintenance costs. Additionally, real estate markets can be volatile, so it’s crucial to conduct thorough market research before diving in.

If you’re a hands-on investor willing to put in the time and effort, real estate can be a rewarding investment. Rental income can supplement your retirement income, and the potential for appreciation over time can serve as a hedge against inflation.

Dividend-Paying Stocks

Dividend-paying stocks offer a steady stream of income during your retirement years. When you invest in these stocks, you receive a portion of the company’s profits paid out as dividends. This can provide a consistent income supplement, especially if you reinvest these dividends to grow your portfolio.

Dividend-paying stocks tend to be less volatile than growth stocks, making them a more conservative option for retirement planning. However, the income you receive will depend on the stock’s dividend yield, which can fluctuate based on market conditions.

Annuities

Annuities are insurance contracts that guarantee a stream of payments for the rest of your life, regardless of how long you live. This can provide much-needed peace of mind and stability in retirement. There are different types of annuities available, each with its advantages and drawbacks.

One important consideration with annuities is the surrender penalty. If you need to access your funds before the policy’s maturity date, you may face a stiff penalty. Additionally, annuities can be expensive, and the returns may not be as high as some other investment options.

Precious Metals

Gold and silver have been considered safe-haven investments for centuries. During periods of economic uncertainty, investors often flock to precious metals as a hedge against inflation. However, precious metals can be volatile investments, and their value can fluctuate significantly.

If you choose to invest in precious metals, it’s recommended to do so as part of a diversified portfolio rather than putting all your eggs in one basket. Physical ownership of precious metals can be cumbersome and expensive, so consider investing in ETFs or mutual funds that track their prices.

Private Equity

Private equity investments involve investing in companies that are not publicly traded. These investments can potentially offer higher returns than traditional stock investments, but they also come with higher risks. Private equity investments are typically reserved for accredited investors who have the experience and expertise to assess these investments.

Private equity can be a good option for investors seeking higher returns and willing to take on more risk. However, these investments are often illiquid, meaning it can be challenging to access your funds if you need them.

No responses yet