Biggest Financial Mistakes That Young Adults Make

1. Living Beyond Your Means

Living beyond your means is one of the biggest financial mistakes that young adults make. When you live beyond your means, you spend more money than you earn. This can lead to credit card debt, personal loans, and other financial problems.

There are a number of reasons why young adults might live beyond their means. Some young adults may not have a good understanding of personal finance. They may not know how to budget, or they may not realize how much things cost. Other young adults may simply be too tempted to spend money. They may see something they want, and they buy it without thinking about whether or not they can afford it.

Whatever the reason, living beyond your means is a dangerous financial habit. It can lead to a number of problems, including:

* Credit card debt

* Personal loans

* Payday loans

* Bankruptcy

If you’re living beyond your means, you need to take steps to change your spending habits. Start by creating a budget. This will help you track your income and expenses, and it will show you where you’re spending too much money. Once you know where you’re spending too much, you can start to make changes.

Here are a few tips for living within your means:

* Create a budget

* Track your spending

* Cut back on unnecessary expenses

* Find ways to earn extra money

2. Not Saving for Retirement

Another big financial mistake that young adults make is not saving for retirement. Retirement may seem like a long way off, but it’s never too early to start saving. The sooner you start saving, the more money you’ll have when you retire.

There are a number of different ways to save for retirement. You can open a traditional IRA, a Roth IRA, or a 401(k) plan. If your employer offers a 401(k) plan, you should definitely take advantage of it. Your employer may even match your contributions, which is free money!

No matter how much you can save, start saving for retirement today. You’ll be glad you did when you’re older.

3. Ignoring Your Credit

Your credit score is a number that lenders use to determine whether or not to lend you money. A good credit score will help you get approved for loans, credit cards, and other financial products. A bad credit score will make it difficult to get approved for loans, and you may have to pay higher interest rates.

There are a number of things you can do to improve your credit score. Pay your bills on time, every time. Keep your credit utilization low, and don’t open too many new credit accounts in a short period of time.

Monitoring your credit is also important. You can get a free copy of your credit report from each of the three major credit bureaus once per year. Review your credit report carefully, and dispute any errors.

The Biggest Financial Mistakes Young Adults Make

Ah, the trials and tribulations of being a young adult. It’s a time of newfound freedom, independence, and… financial blunders. If you’re not careful, you could end up making some costly missteps that will haunt you for years to come. Let’s dive into the biggest financial mistakes young adults often make and how to avoid them.

Not having a budget

A budget is your financial roadmap, helping you track your income and expenses. Without one, it’s easy to fall into the trap of spending more than you earn. Creating a budget is not rocket science; it’s just a matter of writing down your income and allocating it to various categories like rent, food, and entertainment. Once you have a budget, stick to it as much as possible. It’s like having a financial GPS, guiding you towards financial security.

Putting all your eggs in one basket

Investing is a smart way to grow your money over time. But don’t make the mistake of putting all your eggs in one basket. Diversify your investments by spreading them across different asset classes, such as stocks, bonds, and real estate. That way, if one investment takes a hit, you won’t lose everything. It’s like building a financial portfolio that’s weather-proof against market storms.

Ignoring your credit score

Your credit score is like your financial reputation. It can affect everything from your ability to get a loan to the interest rate you pay on your credit card. Don’t ignore your credit score. Check it regularly and take steps to improve it, such as paying your bills on time, keeping your credit utilization low, and avoiding unnecessary credit inquiries. A good credit score is like a golden ticket, opening doors to better financial opportunities.

Living beyond your means

It’s tempting to live the high life when you’re young and have a steady paycheck. But beware of the dangers of living beyond your means. Don’t spend more than you earn, and don’t accumulate unnecessary debt. Remember, debt is like a heavy backpack, weighing you down and making it harder to reach your financial goals.

Not planning for retirement

Retirement may seem like a distant reality, but it’s never too early to start planning. The sooner you start saving for retirement, the more time your money has to grow. Start by contributing to a 401(k) or IRA, even if it’s just a small amount. It’s like planting a seed that will grow into a mighty financial tree in the future.

Biggest financial mistakes that young adults make

Money can be a tricky thing to manage, especially when you’re young and just starting out. There are so many things to spend it on, and it can be tough to know what’s worth your hard-earned cash. That’s why it’s important to avoid any big financial mistakes. So what are they? Here are a few of the most common financial mistakes that young adults make, and how to avoid them.

Chasing get-rich-quick schemes

If something sounds too good to be true, it probably is. There’s no such thing as easy money. If someone is promising you a quick and easy way to make a lot of money, be very skeptical. Chances are, it’s a scam.

Instead of chasing get-rich-quick schemes, focus on building your financial foundation. This means saving money, investing in yourself, and making smart financial decisions.

Not saving money

One of the biggest financial mistakes that young adults make is not saving money. Even if you’re only saving a small amount each month, it can add up over time. Start saving early and you’ll be glad you did when you’re older.

Spending too much money on unnecessary things

Another common mistake is spending too much money on unnecessary things. This can include things like eating out too often, buying clothes you don’t need, or going on expensive vacations.

Instead of spending money on things you don’t need, focus on saving for the things that are important to you. This could include buying a house, starting a family, or retiring early.

Not planning for the future

It’s important to start planning for the future as early as possible. This means setting financial goals, creating a budget, and investing for the long term.

The sooner you start planning for the future, the more time your money has to grow. This will help you reach your financial goals sooner and live a more comfortable life in the future.

Ignoring your credit score

Your credit score is a number that lenders use to assess your creditworthiness. A good credit score can help you get approved for loans, credit cards, and other financial products. A bad credit score can make it difficult to borrow money and can even cost you more money in the long run.

It’s important to start building good credit habits as early as possible. This means paying your bills on time, every time. It also means keeping your credit utilization ratio low.

The Biggest Financial Mistakes That Young Adults Make

Young adulthood is a time of great change and opportunity. It is also a time when many people make financial mistakes that can have long-term consequences. Here are the seven biggest financial mistakes that young adults make:

1. Not saving enough money

Saving money is essential for financial security. When you’re young, it’s easy to think that you have plenty of time to save for retirement. But the sooner you start saving, the more money you’ll have in the long run. Try to save at least 10% of your income each month. This may seem like a small amount, but it can add up over time.

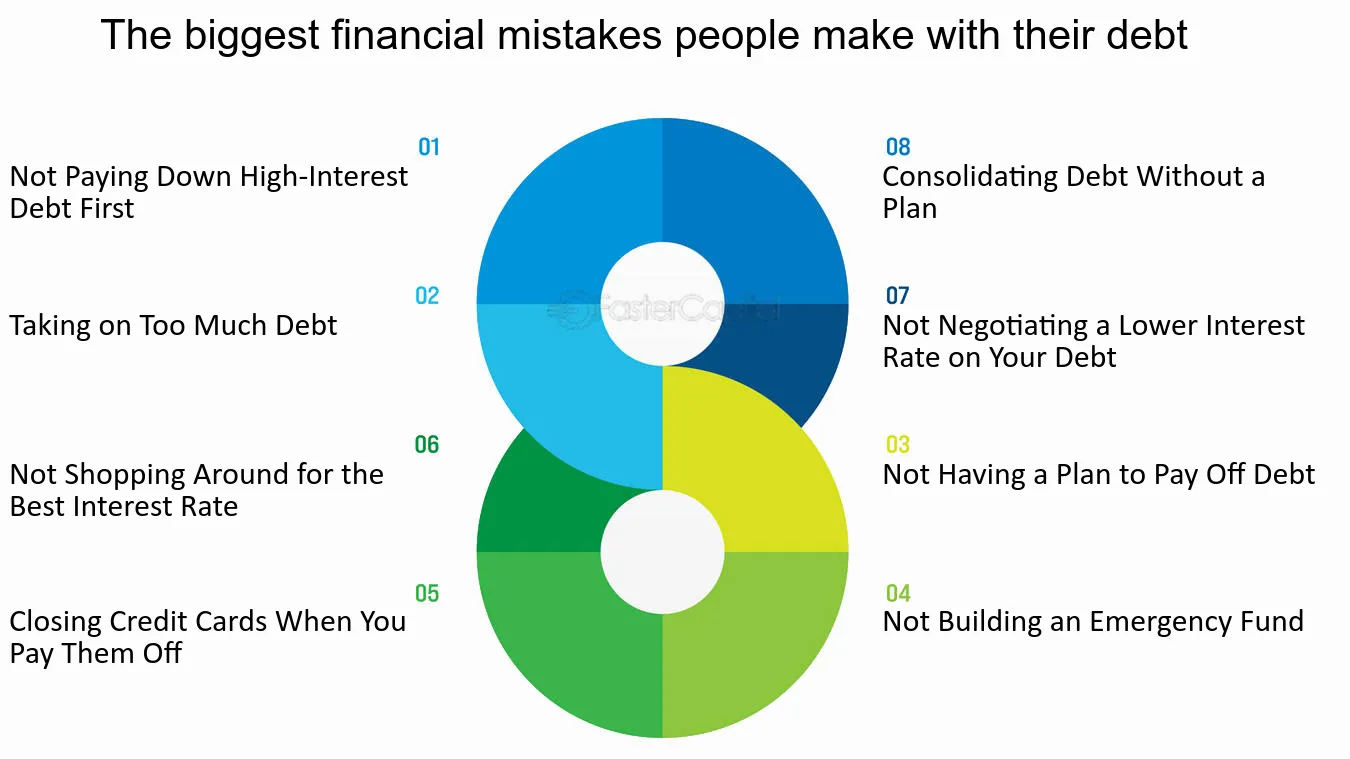

2. Taking on too much debt

Debt can be a major burden, especially for young adults. Avoid taking on too much debt by only borrowing what you can afford to repay.

If you have a lot of debt, it’s important to make a plan to pay it down as quickly as possible. There are several ways to do this, such as increasing your income, cutting your expenses, or consolidating your debt.

Credit card debt is particularly dangerous, as it can quickly spiral out of control. If you’re struggling to pay off your credit card debt, you should seek professional help as soon as possible.

3. Not investing your money

Investing is one of the best ways to grow your wealth over time. However, many young adults are hesitant to invest because they don’t have a lot of money to spare. Even if you can only invest a small amount of money each month, it will add up over time and help you reach your financial goals sooner.

There are many different ways to invest your money, and the best option for you will depend on your individual circumstances and financial goals. You should consider working with a financial advisor to create an investment plan that suits your needs.

4. Not understanding the fine print

When you’re signing a contract for a loan, a credit card, or even a cell phone plan, it’s important to read the fine print carefully. This is where the hidden fees and penalties are usually hiding.

If you don’t understand something in the fine print, don’t be afraid to ask questions. It’s better to be clear about what you’re signing up for before you put your name on the dotted line.

Here are some examples of hidden fees that you should watch out for:

By understanding the fine print, you can avoid these fees and protect your finances.

5. Not building credit

Building credit is important for many reasons. It can help you get approved for loans, get lower interest rates, and even get a job.

There are several ways to build credit. One way is to get a credit card and use it responsibly. Another way is to take out a small loan and make your payments on time.

If you don’t have any credit history, you can start by getting a secured credit card. This type of credit card requires you to put down a security deposit, which is typically equal to the amount of your credit limit.

Once you have a credit card, it’s important to use it responsibly. This means paying your bills on time and not overspending.

**Biggest Financial Mistakes That Young Adults Make: A Financial Pitfalls and Potential Solutions**

Financial planning in young adulthood can lay the foundation for a secure financial future. However, common pitfalls can hinder financial success. Let’s dive into some of the biggest financial mistakes young adults make and explore ways to mitigate these errors.

**1. Not saving for retirement**

Retirement may seem distant, but starting a retirement plan early is crucial. Even small contributions now can accumulate significantly over time, and compound interest can work wonders.

**2. Not building an emergency fund**

Unforeseen expenses can arise at any moment. Having an emergency fund provides a financial cushion to cover unexpected costs, preventing high-interest debt or dipping into retirement savings. Aim for at least 3-6 months’ worth of living expenses.

**3. Not tracking expenses**

Keeping track of your spending habits is essential for financial control. Use budgeting apps or simply record your transactions in a spreadsheet. Understanding where your money goes empowers you to make informed financial decisions.

**4. Renting instead of buying (in some cases)**

For many young adults, renting is a viable option. However, in some markets, long-term renting may end up being more expensive than purchasing a home. Consider factors such as mortgage rates, property taxes, and potential appreciation before making a decision.

**5. Not investing in yourself**

Investing in your education, skills, and professional development can pay dividends in the long run. Whether it’s pursuing higher education, attending industry conferences, or simply reading industry-related books, investing in yourself enhances your earning potential and career trajectory.

**6. Ignoring the power of compound interest**

Compound interest is a financial superpower. It allows your investments to grow exponentially, even if you don’t add any additional funds. Start investing early and let the magic of compound interest work its wonders.

**7. Not planning for health care costs**

Health care expenses can add up quickly, especially in later life. Consider setting aside funds for future medical costs or purchasing health insurance to cover unexpected expenses.

**8. Not taking advantage of tax-advantaged accounts**

IRA (Individual Retirement Accounts) and 401(k) plans offer tax benefits that can help grow your retirement savings. Take advantage of these accounts by contributing as much as you can afford.

**9. Falling for financial scams**

Financial scams target people of all ages, but young adults can be particularly vulnerable. Be wary of unsolicited investment offers, pyramid schemes, and phishing emails. Do your research and trust only reputable financial advisors.

**10. Not seeking professional financial advice**

If you’re overwhelmed by your finances or unsure of where to start, consider seeking professional financial advice from a certified financial planner. They can help you develop a tailored financial plan that meets your specific needs and goals.

Biggest Financial Mistakes That Young Adults Make

When you’re young and just starting out, it’s easy to make financial mistakes. You may not have a lot of experience managing money, and you may not be aware of all the pitfalls that can trip you up. That’s why it’s important to learn about personal finance and make informed decisions about your money. By avoiding these common mistakes, you can set yourself up for financial success.

Making poor financial decisions

One of the biggest financial mistakes that young adults make is making poor financial decisions. This can include things like borrowing too much money, not saving enough money, or investing in risky ventures. If you’re not careful, these mistakes can lead to serious financial problems down the road.

Not saving enough money

Saving money is essential for financial security. It allows you to build a nest egg for the future, cover unexpected expenses, and reach your financial goals. Unfortunately, many young adults don’t save enough money. They may spend too much on things they don’t need, or they may not realize the importance of saving. If you’re not saving enough money, you’re putting your financial future at risk.

Borrowing too much money

Borrowing money can be a useful way to finance a major purchase, such as a car or a house. However, it’s important to borrow only what you can afford to repay. If you borrow too much money, you could end up in debt over your head. Student loans are a common source of debt for young adults. If you’re not careful, these loans can quickly add up and become a major financial burden.

Investing in risky ventures

Investing is a great way to grow your money over time. However, it’s important to invest wisely. If you invest in risky ventures, you could lose all of your money. Young adults are often attracted to risky investments because they offer the potential for high returns. However, it’s important to remember that high returns come with high risks. If you’re not sure about an investment, it’s best to consult with a financial advisor.

Not understanding personal finance

One of the biggest reasons why young adults make poor financial decisions is that they don’t understand personal finance. They may not know how to budget, how to save money, or how to invest. This lack of knowledge can lead to serious financial problems down the road. If you don’t understand personal finance, it’s important to learn. There are many resources available to help you get started, such as books, articles, and websites.

No responses yet